Back to Blog

How to Calculate APY and Maximize Your Returns

Learn how to calculate APY with our practical guide. We break down the formula with real examples to help you compare investments and maximize earnings.

Jul 24, 2025

published

Before you can start calculating APY, you need to get your head around why it's the most honest way to measure your investment's growth. It’s the real rate of return you can expect over a full year. Think of it as a standardized yardstick that lets you fairly compare different financial products, cutting through the marketing fluff.

What APY Actually Means for Your Money

The secret ingredient that makes APY so powerful is compounding. This is where the magic happens. It’s when the interest you earn gets added back to your principal balance, and then that new, bigger balance starts earning interest of its own. It's a snowball effect—your money starts working for you, and then the money it makes also starts working for you.

This cycle is the key to building wealth over time.

The Power of Compounding Frequency

Now, here's where it gets interesting. How often this compounding happens—daily, monthly, or quarterly—makes a huge difference in your total return. The more frequent the compounding, the higher your APY will be, even if the base interest rate is exactly the same as another product's.

This is exactly why you can't just compare simple interest rates.

For instance, a savings account with a 4% rate that compounds daily is going to earn you more than one with the same 4% rate that only compounds quarterly. The APY tells you this story; the base rate doesn't. That’s precisely why you’ll see banks and DeFi protocols advertising APY—it shows off the full earning potential.

APY vs APR: The Key Distinction

It's super easy to mix up APY with its cousin, APR (Annual Percentage Rate). They sound similar, but they are worlds apart and not interchangeable.

APY (Annual Percentage Yield) is all about earning. It factors in compounding to show you how much your money will actually grow.

APR (Annual Percentage Rate) is for borrowing. It shows the annual cost of a loan or credit card debt, but it crucially doesn't show the effect of compounding interest working against you.

In short, you always want a high APY on your savings and investments, and a low APR on your loans and debts. Grasping this simple difference is one of the first and most important steps toward making smarter financial moves.

Whether you're looking at a high-yield savings account, a Certificate of Deposit (CD), or even yields from crypto staking, APY is the universal language for returns. Learning to calculate it for yourself empowers you to see past the big marketing numbers and understand the true earning power of your assets.

The Core APY Calculation Formula Explained

Alright, it's time to pull back the curtain on the math that drives your money's growth. The formula to calculate APY can look a little intimidating at first glance, but it’s a surprisingly simple tool once you get what each part does.

Here it is, in all its glory:

APY = (1 + r/n)ⁿ - 1

This isn't just a random jumble of letters and numbers; it's the engine that reveals how compounding interest truly works on your investments. Let's break it down piece by piece so you can use it confidently.

Decoding the Variables

The real power of this formula comes down to two key variables: 'r' and 'n'. Once you know what they stand for, you’ve unlocked the whole calculation.

r (Nominal Interest Rate): This is just the advertised annual interest rate for whatever you're investing in. It's the percentage you see on the tin, but for the formula, you need to write it as a decimal. So, a 3% rate becomes 0.03. Simple.

n (Number of Compounding Periods): This one's the secret sauce. It represents how many times your interest is calculated and added to your balance within a single year. The more often it compounds, the bigger 'n' gets.

This 'n' value is what really separates APY from a simple interest rate. It's the number that quantifies that compounding magic we talked about earlier.

Compounding Frequencies in Practice

To actually use the formula, you have to know the 'n' value for your specific investment. Most of the time, you'll run into one of these:

Annually: n = 1

Quarterly: n = 4

Monthly: n = 12

Daily: n = 365

Now, let's stop talking theory and put this into action with a real-world example.

Key Takeaway: The annual percentage yield (APY) is the most honest way to measure your return because it includes the effect of compounding. This creates a level playing field, letting you accurately compare different products that might have wildly different compounding schedules.

A Practical Walkthrough

Let's imagine you're eyeing a savings account that's offering a 3% nominal interest rate, and it compounds your interest monthly. How do you figure out the real APY you're going to get?

First up, we grab our variables:

r = 0.03 (that 3% rate, written as a decimal)

n = 12 (because it compounds monthly)

Next, we just plug those numbers into our formula:

APY = (1 + 0.03 / 12)¹² - 1

Let's solve it together, step-by-step:

Divide the rate by the number of periods: 0.03 / 12 = 0.0025

Add 1 to that number: 1 + 0.0025 = 1.0025

Raise it to the power of the periods: (1.0025)¹² is roughly 1.030416

Subtract 1 to get just the yield: 1.030416 - 1 = 0.030416

The final step is to turn that decimal back into a percentage. Boom: you get an APY of 3.04%.

See that? The actual APY is a little bit higher than the advertised 3% rate. That tiny difference is the "free money" you get from having your interest compounded every month instead of just once a year.

For anyone in the crypto space trying to track this across different assets, doing it manually is a nightmare. This is where tools like those in our Yield Seeker terminal become invaluable, helping you track and optimize these returns on the fly.

Putting Your APY Calculation Skills to Work

Knowing the formula is one thing, but actually using it to make smart decisions is how you build wealth. This is where we stop talking theory and start looking at the real-world financial products you'll run into every day.

Being able to calculate APY in these situations is what gives you a real edge. Let's dive into a few examples to see just how much the compounding frequency can change the game.

High-Yield Savings vs. a Certificate of Deposit

Imagine you have some cash to stash and you're weighing two options:

A High-Yield Savings Account (HYSA) with a 4.5% nominal interest rate that compounds daily.

A 5-year Certificate of Deposit (CD) offering the same 4.5% nominal rate, but it only compounds quarterly.

At first glance, they might seem identical. Same rate, right? But the compounding schedule is the real story here.

For the HYSA that compounds daily, our variables are r = 0.045 and n = 365. The math shakes out like this:

APY = (1 + 0.045 / 365)³⁶⁵ - 1 = 4.60%

Now for the CD, which compounds quarterly, our variables are r = 0.045 and n = 4:

APY = (1 + 0.045 / 4)⁴ - 1 = 4.58%

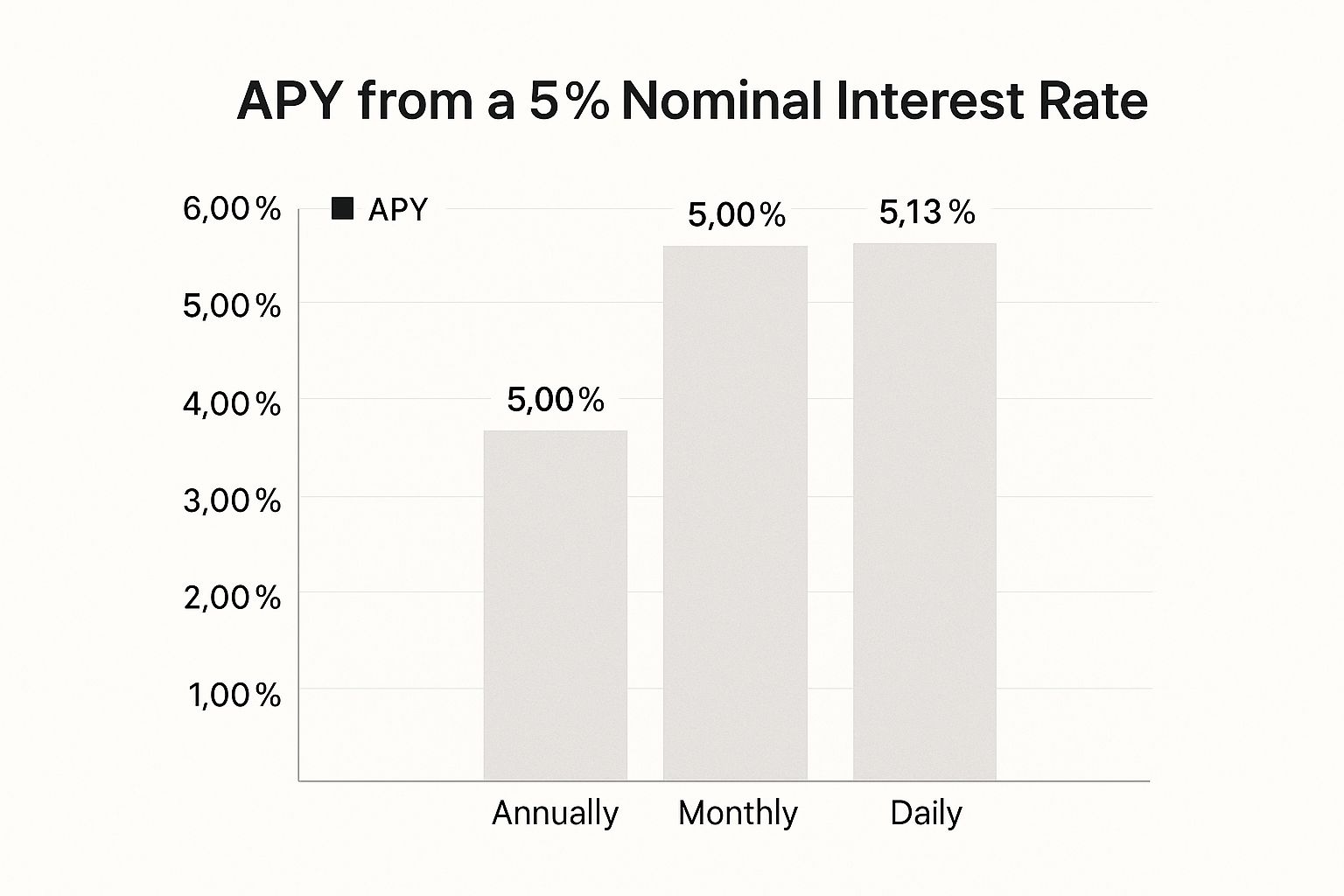

It's a small difference, sure, but it’s not nothing. The daily compounding in the HYSA gives you a clear, albeit slight, advantage in earning power over the year. This visual below perfectly shows how even small increases in compounding frequency give your final return a boost, using a 5% nominal rate as an example.

As you can see, jumping from annual to monthly, and then again to daily compounding, each step up provides a measurable bump in your effective annual yield.

When APY Works Against You

It’s easy to forget that compounding isn't always your friend. When you're on the other side of the equation—dealing with debt—the same principles work in the lender's favor. Think high-interest credit cards. They often advertise an APR, but the interest you're charged is almost always compounded daily.

If your credit card has a 21% APR and compounds daily, your effective annual rate is actually closer to 23.36%. This is exactly why credit card balances can spiral out of control so fast. You're paying interest on your interest every single day.

Understanding this dark side of compounding is just as critical as knowing how to use it for your investments. It’s the reason why paying down high-interest debt should almost always be your top financial priority.

Comparing Investment Outcomes

To really hammer this point home, let's compare two different savings accounts side-by-side. We’ll start with an initial deposit of $10,000 and see what happens after one year.

This table shows exactly how a better APY translates directly into more money in your pocket.

APY Comparison High-Yield Savings vs. Standard Savings

Feature | High-Yield Savings Account | Standard Savings Account |

|---|---|---|

Nominal Interest Rate | 4.50% | 0.45% |

Compounding Frequency | Daily | Monthly |

Calculated APY | 4.60% | 0.45% |

Total Earnings After 1 Year | $460 | $45 |

Ending Balance | $10,460 | $10,045 |

The results are stark. The high-yield account, thanks to its superior rate and more frequent compounding, nets you $415 more in earnings over a single year. That's not pocket change.

This is a powerful demonstration of why you have to look beyond the advertised rate. Calculating the APY is the only reliable way to see the full picture and make sure you're choosing the option that will truly maximize your returns.

Calculating APY in Crypto and DeFi

The same principles we use to calculate APY in a bank are absolutely essential in the world of crypto and Decentralized Finance (DeFi). The big difference? The numbers are often way more exciting.

You'll see terms like staking, liquidity providing, and yield farming thrown around, all promising returns advertised as APY. But crypto APY plays by a different set of rules. Unlike the sleepy, fixed-rate world of traditional finance, DeFi yields are alive. They can swing wildly day-to-day—sometimes even hour-to-hour—based on token prices, how busy a protocol is, and reward schedules. This makes getting a grip on the mechanics even more critical.

Staking Stablecoins: A Practical DeFi Example

Let's walk through one of the most common entry points into DeFi: staking a stablecoin like USDC on a lending platform. The idea is straightforward. You deposit your stablecoins, other people borrow them, and you earn a slice of the interest they pay.

Say you stake $1,000 in USDC on a platform showing a juicy 10% APY. On paper, you’d expect to have $1,100 after a year. But here’s where DeFi throws a few curveballs:

Variable Rates: That 10% APY isn't a promise. It's a snapshot based on current market demand. If borrowing demand dries up, your APY could plummet to 5%. If it spikes, you might see it jump to 15%.

Reward Tokens: A lot of the time, your yield isn't paid back in the USDC you deposited. Instead, you might get the platform's native governance token. This adds a whole new layer of risk because the value of that token can go up or down, dramatically affecting your real return.

Compounding Frequency: In DeFi, rewards often need to be claimed manually. Your true APY hinges on how often you claim those rewards and put them back to work (re-stake them), which is what gets the compounding engine really humming.

The APY you see advertised in DeFi is rarely a "set it and forget it" number. It’s a real-time snapshot of potential earnings. Your actual, realized APY depends on market conditions, your own actions, and the stability of the rewards you receive.

Beyond the Numbers: Risks to Consider

While the potential for high APY in crypto is what draws people in, it comes with specific risks that you just don't see in traditional banking. It's not just about prices going up and down.

First up is smart contract risk. The entire DeFi world is built on code. If that code has a bug or a vulnerability, it can be exploited by hackers, potentially leading to a total loss of your funds. For a deeper dive on this, our guide on safer crypto staking strategies is a great place to start.

Another big one is impermanent loss, a risk that mainly hits people providing liquidity to decentralized exchanges. It’s a tricky concept where you can actually end up with less value than if you had just held your tokens, even if the market is going up.

Ultimately, a sky-high APY in DeFi is almost always your compensation for taking on these extra risks. Your job as an investor is to figure out if the potential reward is worth it.

How Economic Trends Shape Your APY

The APY you see advertised on your savings account or a DeFi dashboard doesn’t just materialize out of thin air. It’s actually a direct reflection of much larger economic forces, connecting your personal finances to what’s happening on the global stage.

Getting a handle on this connection is the key to spotting changes before they happen and tweaking your strategy accordingly.

The Central Bank Connection

At the heart of it all are the central banks, like the U.S. Federal Reserve. When you hear on the news that "the Fed is raising rates," that’s a signal that will eventually ripple all the way down to your savings.

Central banks set the baseline cost of borrowing for the entire economy. When they raise this rate, it gets more expensive for commercial banks to borrow money. To shore up their cash reserves, they turn to you, offering higher APYs on savings products to attract more of your deposits. It’s a simple supply and demand game.

The opposite is also true. When the economy slows down, central banks often slash rates to get people borrowing and spending again. This makes stashing cash less appealing, and as a result, the APYs offered by banks and even DeFi protocols tend to take a nosedive.

A Quick Look at History

History paints a really clear picture of this dynamic. Just look at the historical trends for Certificates of Deposit (CDs).

In the low-interest-rate world of June 2013, a 1-year CD would have earned you a measly 0.24% APY on average. Fast forward to the 2022-2023 period, after the Fed hiked rates 11 times to fight off inflation, and it was easy to find CDs offering APYs well over 4%. You can dig into how these CD rates have shifted over time yourself.

That massive swing shows just how much the economic climate dictates the rewards for saving. An investor who not only knows how to calculate APY but also keeps an eye on these big-picture trends is in a much better spot to pounce when great rates pop up.

Think of the APY on your savings as a thermometer for the economy's health. Rising rates often mean an effort to cool down inflation, making your savings work harder. Falling rates suggest a push for economic growth, which usually means lower returns on your cash.

How to Use This to Your Advantage

So, how do you turn this knowledge into action? It’s all about becoming a more informed investor instead of just a passive saver.

Here’s what I do:

Follow Central Bank News: Pay attention when Fed chairs or other central bank leaders talk. The language they use about inflation and economic growth is packed with clues about where rates might go next.

Anticipate the Moves: If you see inflation running hot and the economy is strong, you can reasonably expect rates (and APYs) to climb. This might be a good time to keep your money in shorter-term savings products, so you can reinvest at even better rates down the road.

Lock in the Highs: Conversely, when APYs are juicy but economists are forecasting a slowdown, that could be the perfect moment. It might be time to lock in that high APY with a longer-term product, like a multi-year CD, before rates start to fall again.

By understanding the 'why' behind APY movements, you shift from being someone who just takes whatever rate is offered to an active player in your own financial story. You're not just reacting anymore—you're anticipating the shifts and putting your money in a position to benefit.

Got APY Questions? Let's Clear Them Up

Even once you get the hang of the APY formula, a few common questions always seem to pop up. Let's tackle them head-on so you can feel totally confident when you're looking at different yield opportunities.

Is APY the Same as APR?

This is easily the biggest point of confusion, and the answer is a hard no. They might sound alike, but they're used for completely different things.

APY (Annual Percentage Yield) is all about earning. It's the one that includes the magic of compounding, showing you the real growth of your money over a year. You want this number to be as high as you can safely get it.

APR (Annual Percentage Rate) is for borrowing. It tells you the yearly cost of a loan or credit card, but it doesn't show you how compounding interest works against you. You want this number to be as low as possible.

Just think of it this way: APY is your best friend when you're saving, while APR is the enemy when you're in debt.

Is a Higher APY Always Better?

Not always. A super high APY should make you pause and ask more questions, not just jump in.

In traditional banking, a higher APY is almost always a good sign—it just means a more competitive savings account. But in the wild world of DeFi, a sky-high APY can sometimes signal higher risk. This could be due to a volatile reward token or an unproven, unaudited protocol.

Your real goal isn't just to chase the highest number, but to find the best risk-adjusted return. A stable 5% APY from a well-known, battle-tested protocol is often a much smarter move than a speculative 500% APY from an anonymous project that just launched last week.

How Do I Handle a Variable APY?

Lots of products, especially high-yield savings accounts and pretty much all DeFi opportunities, come with a variable APY. This just means the rate isn't fixed and can change over time.

It's super important to remember that the advertised APY is just a snapshot of the current rate. It’s not a promise for the whole year.

These rates are often tied to what's happening in the broader economy. Central bank policy rates, for example, set the baseline for what banks and DeFi protocols can offer. You can actually see how these economic shifts impact savings yields globally by tracking the data. For a deeper look, you can explore the evolution of policy rates tracked by the Bank for International Settlements.

When you're dealing with variable rates, it’s a good idea to check in on your returns every so often to see how your APY is trending. Being proactive like this means you'll always know what your real earning potential looks like.

For more tips on navigating the financial world, feel free to check out our other articles over on the Yield Seeker blog.

Ready to put your APY knowledge to work without the manual effort? Yield Seeker uses an AI Agent to automatically find and manage the best stablecoin yields for you. Start earning smarter at https://yieldseeker.xyz.