Back to Blog

Crypto Tax Reporting Requirements Simplified

Master crypto tax reporting requirements with this guide. Learn to navigate IRS forms, calculate gains, and avoid common mistakes for full compliance.

Aug 14, 2025

published

When it comes to taxes, there's one golden rule you have to burn into your brain: the IRS treats cryptocurrency as property, not currency.

This single concept is the key to understanding everything else. Forget thinking about your Bitcoin or Ethereum like the dollars in your bank account. Instead, think of them like stocks, a piece of art, or a rental property.

Once you make that mental shift, the logic of crypto taxes falls into place.

The Foundation of Crypto Tax Reporting

Because crypto is property, nearly every time you get rid of it, you're triggering a taxable event. This is just like selling a stock. You sell, you calculate your profit or loss, and you report it to the IRS.

It's a much broader net than most people realize. A "disposal" of your crypto isn't just selling it on an exchange. It also includes:

Selling crypto for U.S. dollars.

Trading one crypto for another (like swapping ETH for SOL).

Using crypto to buy something, like a cup of coffee or a new laptop.

Earning crypto as income from things like mining, airdrops, or specific types of rewards.

Let's use the coffee example because it really highlights the difference. If you buy coffee with a $5 bill, that's just a simple purchase. No tax impact. But if you pay with $5 worth of Bitcoin? The IRS sees that as two separate events: first, you sold your Bitcoin for $5, and second, you used that $5 to buy the coffee. That "sale" is the part you have to report.

Short-Term vs. Long-Term Gains

Okay, so you've made a trade and have a gain. The next question is, how long did you hold the asset? This is a huge deal because it directly impacts your tax rate.

Honestly, the difference between short-term and long-term gains is one of the most powerful tools you have for tax planning. Holding an asset for just over a year can literally cut your tax bill in half. This is the government's way of rewarding patient, long-term investors over frequent traders.

A short-term capital gain is from selling crypto you held for one year or less. These profits are taxed at your regular income tax rate, which can be as high as 37%. Ouch.

A long-term capital gain, on the other hand, applies to assets you've held for more than one year. The tax rates here are way friendlier: 0%, 15%, or 20%, depending on your total income.

To help you keep track, here's a quick rundown of some common activities and how they're generally treated for tax purposes.

Key Crypto Activities and Their Tax Implications

This table summarizes which common crypto transactions are typically considered taxable events that you need to report to the IRS.

Crypto Activity | Is it a Taxable Event? | Primary Reporting Form |

|---|---|---|

Selling Crypto for Fiat (e.g., USD) | Yes | Form 8949 / Schedule D |

Trading Crypto for Crypto (e.g., BTC for ETH) | Yes | Form 8949 / Schedule D |

Using Crypto to Buy Goods/Services | Yes | Form 8949 / Schedule D |

Receiving Crypto as Payment for Work | Yes (Income) | Schedule C or Schedule 1 |

Airdrops | Yes (Income) | Schedule 1 |

Mining Rewards | Yes (Income) | Schedule C or Schedule 1 |

Buying Crypto with Fiat (e.g., USD) | No | Not applicable |

Holding Crypto (HODLing) | No | Not applicable |

Donating Crypto to a Qualified Charity | No | Form 8283 (if over $500) |

Gifting Crypto to Someone | No (up to annual limit) | Form 709 (if over limit) |

Remember, this is a general guide. Your specific situation might have unique nuances, but for most people, this covers the major bases for reporting capital gains and losses.

Evolving IRS Rules and Forms

The crypto world moves fast, and the tax rules are trying their best to keep up. The IRS is getting much more serious about enforcement, so being sloppy with your reporting is no longer an option.

For the 2024 tax year, you'll primarily be using Form 8949 to detail each individual transaction and then summarizing the totals on Schedule D. If you earned crypto as income, that will likely go on Schedule 1 or Schedule C. While it’s not in effect yet, be aware that the IRS is also developing a new Form 1099-DA. The plan is for crypto exchanges to use this form to report your transaction data directly to the IRS, similar to how stockbrokers do. This could become mandatory as early as 2026 for the 2025 tax year.

Since different types of crypto income have their own specific rules, it's a good idea to dig into the details. For example, if you're earning yield, you should review the specific guidance on how are staking rewards taxed. Staying informed is your best defense against a surprise tax bill.

Identifying Your Taxable and Non-Taxable Events

Okay, so we've established the first big rule: the IRS sees your crypto as property. The next crucial step is learning to spot exactly which of your activities ring the tax bell and which ones fly completely under the radar.

Getting this right is the absolute bedrock of accurate crypto tax reporting. It might seem like a lot to track, but once you get the hang of it, you’ll start seeing the patterns. The core idea is simple: a taxable event usually happens whenever you dispose of your crypto—basically, when you get rid of it in exchange for something else of value.

Common Taxable Events You Must Report

Think of these as the specific moments you absolutely need to capture for your tax records. Each one creates a potential capital gain or loss that has to be calculated and eventually reported on your tax return.

Selling Crypto for Fiat Currency: This is the most obvious one. If you sell 1 ETH for $3,000 in cash, you've disposed of your asset. That's a taxable event, plain and simple.

Trading One Crypto for Another: This trips up so many people. Swapping your Bitcoin for Solana isn't like trading a blue car for a red one. The IRS views it as two separate transactions: you technically "sold" your Bitcoin and then immediately used that money to buy Solana. That initial sale of Bitcoin is a taxable event.

Using Crypto to Buy Goods or Services: Remember that famous story about the guy who bought two pizzas for 10,000 Bitcoin? Every time you buy a coffee, a new laptop, or a subscription with crypto, you're doing the same thing. You're effectively "selling" your crypto for whatever the fair market value of that item is at that exact moment.

Earning Crypto Income: This one is a bit different because it’s usually treated as ordinary income, not a capital gain, but it's still taxable. When you receive crypto from staking, airdrops, mining, or as payment for work, you owe income tax on its market value at the time you received it.

These actions are the bread and butter of what you need to track. Every time you do one of these things, you create a new data point for your tax spreadsheet.

Trading one crypto for another is treated as a sale, not a simple swap, creating a reportable event. This is one of the most misunderstood parts of crypto tax law and a huge reason why people accidentally underreport their taxes.

Activities That Are Typically Non-Taxable

Just as important is knowing what doesn't create a tax headache. Recognizing these scenarios will save you a ton of time and unnecessary stress.

The common thread here? You're still in full control of the asset and haven't actually disposed of it.

Non-Taxable Scenarios to Know

These are common moves that generally don't need to be reported as a disposal on your tax return.

Buying Crypto with Fiat Currency: Purchasing Bitcoin with U.S. dollars is just an acquisition. You're not getting rid of anything; you're just establishing your position. Your tax journey starts here, but the taxable event clock doesn't begin ticking until you sell, trade, or spend that crypto.

Holding Your Crypto (HODLing): This is a big one. Simply holding onto your crypto, no matter how much its value skyrockets or plummets, is not a taxable event. Those are all "unrealized" gains or losses. They don't become real in the eyes of the IRS until you actually make a move.

Moving Crypto Between Your Own Wallets: Shifting your ETH from a Coinbase account to your personal Ledger wallet is like moving cash from your checking account to your savings account. You still own it, you've just changed its location. No disposal means no tax event.

Gifting Crypto (Under the Annual Limit): You can gift crypto to someone else without it being a taxable event for you, as long as the value is below the annual gift tax exclusion. For 2024, that limit is $18,000 per person. The person who receives the gift doesn't owe tax on it either, but they do inherit your original cost basis.

Once you can confidently sort your transactions into these two buckets—taxable and non-taxable—you're well on your way. By focusing only on the events that actually matter, you can make your record-keeping way more efficient and meet your tax obligations without getting lost in the weeds.

How to Navigate Essential IRS Crypto Tax Forms

Let's be honest, staring at a stack of tax paperwork feels a lot like trying to decipher a foreign language. But once you get the hang of what each form is actually for, the whole process starts to click into place. Meeting your crypto tax obligations really just boils down to a few key documents.

Think of your annual tax return as the final report for a massive project. Each individual form is like a chapter telling a specific part of your financial story for that year. For crypto investors, the main plot is all about your capital gains and losses.

Form 8949: The Transaction Log

The absolute star of the show for anyone trading crypto is Form 8949, Sales and Other Dispositions of Capital Assets. This form is your detailed, line-by-line transaction log. It’s where you list every single time you sold, traded, or otherwise disposed of your cryptocurrency during the tax year.

For every single transaction, you need to lay out the specifics:

The name of the crypto you sold (e.g., Bitcoin)

The date you first acquired it

The date you sold or traded it away

Your sale price, or the fair market value in USD when you made the transaction

Your cost basis (what it cost you to acquire it, including any fees)

The resulting gain or loss

So, if you sold 0.5 BTC, that's a single line item on Form 8949. You’d detail the exact date you bought that specific 0.5 BTC, the date you sold it, how much cash you got for it, and what you originally paid. This level of detail isn't optional; it's the foundation of your entire crypto tax report.

Think of Form 8949 as the "receipts" for your tax return. It's not enough to just declare, "I made $1,000 on crypto." This form is how you show your work, proving exactly how you arrived at that number with a clear, organized list of every trade.

Schedule D: The Grand Summary

After you've meticulously listed every transaction on Form 8949, you need to tally up the score. That’s where Schedule D, Capital Gains and Losses, comes into play. This form acts as the high-level summary.

You simply take the totals from Form 8949—your total short-term gains and losses, and your total long-term gains and losses—and carry them over to Schedule D. This form then combines your crypto activity with any other capital gains you might have, like from selling stocks. The final number from Schedule D is what ultimately gets reported on your main tax return, Form 1040.

This kind of formal reporting is becoming the global standard. As of 2025, more and more countries are tightening their tax policies. In the U.S. alone, an estimated 65% of crypto investors reported their activities on Form 8949 in 2024. That's a huge jump from just 50% the year before, signaling a major shift toward compliance. For a deeper dive into these global trends, check out the latest research on crypto taxation laws and statistics.

Other Key Forms and Questions

While Form 8949 and Schedule D handle your trading, other crypto activities have their own place on your tax return. If you earned crypto as income—whether from staking rewards, mining, or an airdrop—you’ll report that on Schedule 1 (Form 1040) under "Other income."

Finally, whatever you do, don't miss the big question right at the top of Form 1040. The IRS now asks every single taxpayer: "At any time during [the tax year], did you: (a) receive (as a reward, award, or payment for property or services); or (b) sell, exchange, or otherwise dispose of a digital asset (or a financial interest in a digital asset)?"

Answering this question correctly is a critical first step. If you did anything we've talked about—sold, traded, spent, or earned crypto—you must check "Yes." Ticking "No" when you should have said "Yes" is a massive red flag for the IRS and could lead to some pretty serious headaches down the road.

How to Calculate Your Crypto Gains and Losses

Figuring out your gains and losses is easily the most critical—and often most intimidating—part of handling your crypto taxes. This is where the rubber meets the road, but the process is a lot more straightforward than you might think once you get your head around the concept of cost basis.

Think of your cost basis as the total, all-in price tag for getting your crypto. It's not just the sticker price; it includes all the little extras like exchange fees or network gas fees. Getting this number right is the bedrock of accurate tax reporting, because it's what you subtract from your sale price to find out if you made a profit or a loss.

The basic formula is dead simple:

Sale Price - Cost Basis = Capital Gain or Loss

If you get a positive number, you've got a capital gain. If it's negative, that's a capital loss, which can often be used to offset other gains.

Understanding Accounting Methods

Where things get a bit tricky is when you've bought the same crypto at different prices over time. Say you bought 1 Bitcoin at $30,000 and another at $50,000. If you sell one, which one did you sell? The accounting method you pick determines the answer, and your choice can have a huge impact on your tax bill.

The two most common methods the IRS allows are:

First-In, First-Out (FIFO): This is the default. It assumes the first coins you ever bought are the first ones you sell. It’s simple to track but can sometimes lead to a bigger tax bill in a bull market.

Specific Identification (Spec ID): This method lets you cherry-pick which specific batch of coins you're selling. It demands meticulous records but gives you the most flexibility to manage your tax outcome. It’s a key part of strategic cryptocurrency portfolio rebalancing.

Let’s walk through a quick story to see how this plays out in the real world.

A Tale of Two Tax Outcomes

Imagine an investor named Alex. He made two Bitcoin purchases:

January 1: Bought 1 BTC for $40,000.

June 1: Bought 1 BTC for $60,000.

On December 15, Alex decides to sell 1 BTC for $70,000. The sale price is clear, but his cost basis is a different story depending on the accounting method.

Scenario 1: Using the FIFO Method

With FIFO, the IRS assumes Alex sold the first Bitcoin he bought way back in January.

Sale Price: $70,000

Cost Basis (from Jan 1 purchase): $40,000

Capital Gain: $70,000 - $40,000 = $30,000

Under FIFO, Alex has a taxable gain of $30,000 to report for the year.

Scenario 2: Using the Specific Identification Method

With Spec ID, Alex has a choice. To keep his immediate tax bill as low as possible, he decides to "sell" the coin he bought for a higher price.

Sale Price: $70,000

Cost Basis (from June 1 purchase): $60,000

Capital Gain: $70,000 - $60,000 = $10,000

By using Spec ID, Alex's taxable gain is just $10,000—a whopping $20,000 less than with FIFO! This example shows just how much your chosen method can swing your tax liability. The only catch is consistency; once you pick a method for a specific crypto, you generally have to stick with it.

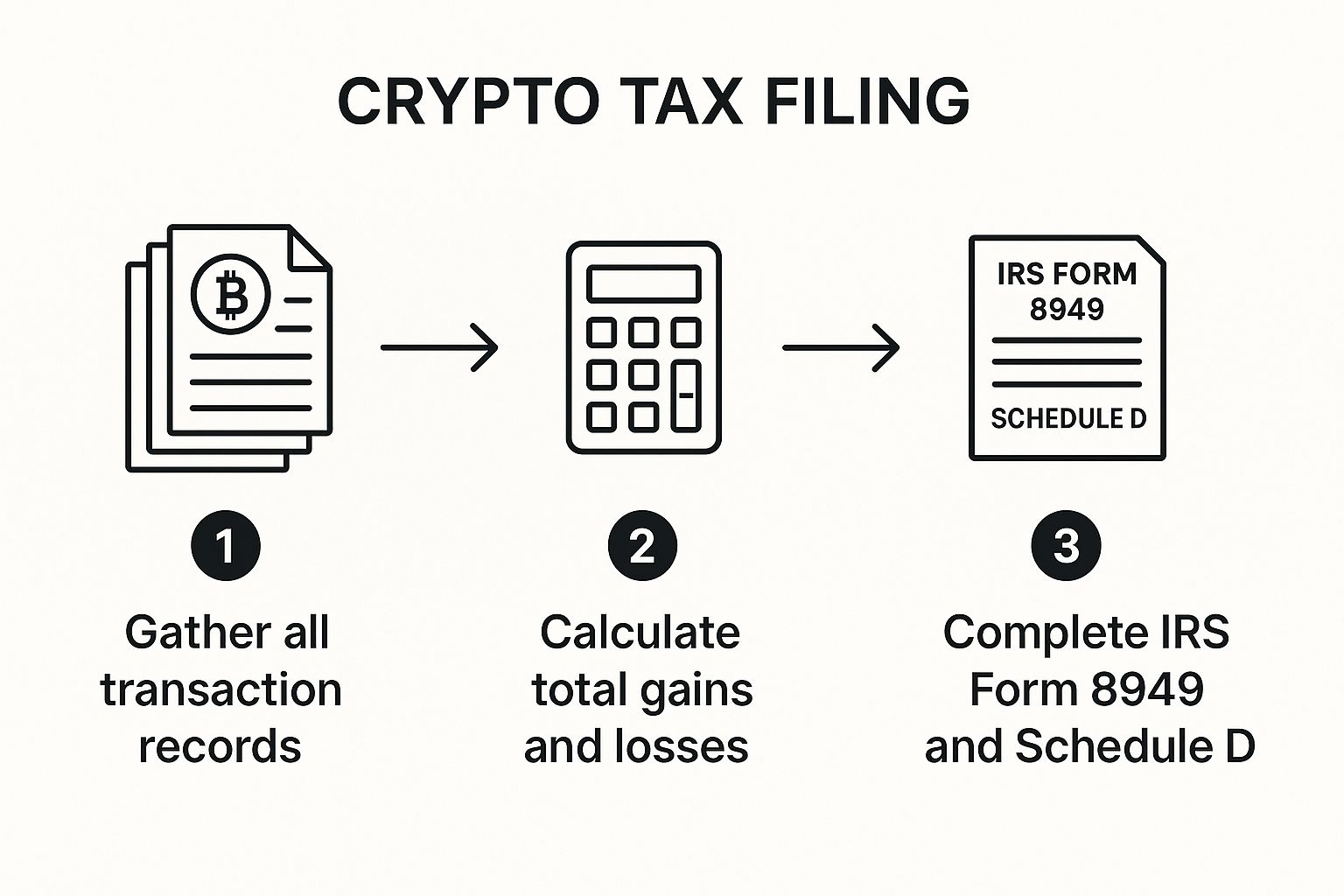

This infographic breaks down the general workflow for crypto taxes, from gathering records to filing the right forms.

As you can see, calculating your gains and losses is the most number-heavy step, bridging the gap between your transaction history and what you actually report to the IRS.

There’s no getting around it: accurate calculations are non-negotiable. The IRS wants to see your work, which is impossible without a clear cost basis and a consistent accounting method. Whether you go with the simplicity of FIFO or the strategic edge of Spec ID, keeping detailed records is your best weapon for avoiding overpayment and staying compliant.

Building Your System for Crypto Record-Keeping

Getting your crypto taxes right doesn't start in April when everything is due. It's a year-round habit built on a solid foundation of great record-keeping.

Let's be honest, scrambling at the last minute to piece together a year's worth of trades is a surefire recipe for stress and mistakes. If you build a simple system now, you can turn tax season into an organized process instead of a panic-filled mess.

The heart of any good system is tracking the right information for every single transaction. Without these key details, it's flat-out impossible to accurately figure out your gains and losses.

The Essential Data for Every Transaction

Think of this as your non-negotiable checklist. Every time you sell, trade, or spend your crypto, you need to grab the following details:

The Asset: Which specific cryptocurrency was it? (e.g., Bitcoin, Ethereum)

Transaction Dates: The exact date you acquired the asset and the exact date you got rid of it.

Fair Market Value: The U.S. dollar value of the crypto at the precise moment of the transaction.

Your Cost Basis: The total amount you paid to get the asset, including any fees you paid to acquire it.

Transaction Fees: Any fees paid when you sold or traded the crypto.

Nailing down these five data points gives you everything you need to satisfy the IRS's crypto tax reporting requirements and fill out Form 8949 without breaking a sweat.

A well-organized record-keeping system is your single best defense against overpaying on your taxes. It provides the proof needed to calculate your cost basis correctly and take advantage of any potential tax-saving strategies, like specific identification.

Choosing Your Record-Keeping Method

Okay, so you know what to track. The next logical question is how. There are a few ways to go about it, each with its own pros and cons. The best method for you really depends on how often you're trading and how complex your activity is.

Someone who only buys crypto a couple of times a year might get by just fine with a simple spreadsheet. But if you're an active DeFi user or a frequent trader, you're almost certainly going to need something more automated.

Let's break down the most common approaches.

Record-Keeping Methods Comparison

Deciding how to track your crypto can feel overwhelming, but this table should help you figure out the best fit for your activity level. It compares the main methods people use, from simple manual tracking to powerful automated software.

Method | Best For | Pros | Cons |

|---|---|---|---|

Manual Spreadsheets | Hobbyists and infrequent traders with a low volume of transactions. | No cost; full control over your data. | Extremely time-consuming; high risk of manual error; not scalable. |

Exchange-Provided Reports | Users who trade exclusively on one or two centralized exchanges. | Easy to download; already formatted. | Often incomplete; don't track transfers or DeFi activity; can be inaccurate. |

Specialized Tax Software | Active traders, DeFi users, and anyone with transactions on multiple platforms. | Automates data aggregation; calculates gains/losses; generates tax forms. | Subscription cost; requires initial setup to sync all wallets and accounts. |

For anyone with more than a handful of transactions, specialized crypto tax software quickly becomes a necessity. These platforms connect directly to your exchanges and wallets via API, automatically pulling in and categorizing your entire transaction history.

This kind of automation doesn't just save you countless hours of mind-numbing data entry; it also dramatically cuts down on the risk of human error. This ensures your crypto tax reporting requirements are met with precision, giving you peace of mind when you file.

Avoiding Common and Costly Reporting Pitfalls

When it comes to crypto taxes, a little bit of knowledge can save you a world of hurt. The landscape is genuinely tricky, and I've seen even savvy investors get tripped up by a few common—and very costly—mistakes. Knowing what these pitfalls are is your best defense against penalties, interest, and the headache of an IRS audit.

The single most frequent error? It's surprisingly simple: forgetting to report crypto-to-crypto trades. Many people fall into the trap of thinking that if no dollars hit their bank account, then there's no taxable event. That's a huge misconception. Swapping your Bitcoin for Ethereum is a reportable sale, and leaving it off your return is a major red flag for the IRS.

Another classic mistake is messing up your cost basis by ignoring transaction fees. Every fee you pay to buy a crypto asset should be added to its cost basis. Forgetting to do this inflates your calculated gains, meaning you end up overpaying on your taxes. It's like giving the government a bigger tip than you need to.

Overlooking Unconventional Income Sources

The crypto world is a lot more than just buying and selling on an exchange, and your tax obligations follow suit. A lot of investors completely overlook the income they're generating from less obvious activities, especially in the wild west of decentralized finance (DeFi). This oversight can snowball into a pretty significant compliance problem.

Here are a few of the usual suspects that often go unreported:

Airdrops: Getting free tokens might feel like a gift, but the IRS sees it as income. The fair market value of those tokens at the moment they land in your wallet is taxable.

Staking and Liquidity Pool Rewards: That yield you're earning from staking your assets or providing liquidity to a protocol? It's all taxable income, valued at the time you receive it.

Lending Interest: Any interest you earn from lending out your crypto on a DeFi platform is another stream of income that needs to be reported.

These income sources can be a real pain to track. It's why any solid approach to DeFi risk management absolutely must include a plan for tax record-keeping. Ignoring it is just asking for trouble.

The Consequences of Non-Compliance

Let's be clear: failing to report accurately isn't a minor slip-up. The consequences are real and they have teeth. The IRS can hit you with failure-to-file penalties, accuracy-related penalties that can be as high as 20% of your underpayment, and of course, interest charges on whatever you owe. An audit is not just time-consuming; it's incredibly stressful.

The global push for crypto tax compliance is only getting stronger. While adoption is booming—with nearly 28% of American adults expected to own crypto by 2025—it's estimated that less than 2% of global investors are fully compliant. You can bet regulators are laser-focused on closing that gap.

Governments everywhere are tightening the screws on crypto taxation. Just look at Italy, where the crypto gains tax is set at 26% and is expected to climb. This shows a clear trend toward more aggressive oversight. The best way to navigate this is to stop thinking of accurate reporting as a chore and start seeing it as a fundamental part of your investment strategy. That's how you file with confidence.

Frequently Asked Questions

When you're dealing with crypto taxes, a few tricky questions always seem to pop up. Even if you've got the basics down, some of the edge cases can leave you scratching your head. Let's walk through some of the most common ones investors run into.

Do I Have to Report Crypto If I Lost Money?

Yes, you absolutely do. The IRS wants to know about all of your crypto sales, trades, or purchases—not just the profitable ones. But this isn't just about following the rules; it's actually a huge opportunity for you.

When you report your losses, you can use them to cancel out capital gains from other investments, which could seriously lower your tax bill. And if your losses are bigger than your gains, you can even deduct up to $3,000 of those losses from your regular income. Anything left over just rolls forward to help you out in future years.

Think of it this way: not reporting your losses is like finding a gift card and throwing it in the trash. It's real money you're leaving on the table. The only way to claim that benefit is to report every single transaction, wins and losses alike.

What Happens If I Receive Crypto as a Gift?

Good news—getting crypto as a gift isn't a taxable event for you, the person receiving it. You won't owe any tax just for having it land in your wallet. The tax part only kicks in when you eventually decide to sell, trade, or spend it.

But here's the catch: to figure out your capital gain or loss later, you need to know the original owner's cost basis (what they paid for it) and the date they bought it. You essentially inherit their tax situation. That's why it's so important to ask the person who gifted you the crypto for this info right away and keep a solid record of it. Without those details, you're flying blind when it's time to file.

Are Crypto Transaction Fees Deductible?

This is a common point of confusion. You can't just list out all your gas fees as a separate deduction like you would with other business expenses. Instead, the IRS has you bake those fees directly into your profit-and-loss calculations for each trade.

It works in two main ways:

When you buy: Any fees you pay to acquire crypto get added to your cost basis. This bumps up the total "cost" of your investment.

When you sell: Fees you pay to sell or trade crypto are subtracted from your total sale proceeds.

By doing it this way, you naturally reduce your taxable gain (or increase your reportable loss). It ensures you’re only paying tax on what you actually profited from the transaction, which is exactly how it should be.

Are you looking for a simpler way to grow your stablecoin holdings without the constant research? With Yield Seeker, you can put your USDC to work on the BASE chain effortlessly. Our AI-driven platform finds and manages the best yield opportunities for you, so you can earn passive income around the clock. Get started in seconds and watch your yield grow. Discover a smarter way to earn at https://yieldseeker.xyz.