Back to Blog

Understanding Stablecoin Interest Rates

Unlock the world of DeFi passive income. This guide explains stablecoin interest rates, how they work, the risks involved, and strategies to earn.

Jul 25, 2025

published

So, what are stablecoin interest rates? Simply put, they're the returns you can get by lending out your digital dollars on decentralized finance (DeFi) platforms. The yields are often much, much higher than what you’d see in a traditional bank account.

Think of it like a global, automated peer-to-peer lending market that never sleeps, all powered by code instead of bankers.

Your Guide to Earning With Stablecoins

In this marketplace, you can lend your stablecoins—crypto assets pegged to a real-world currency like the U.S. dollar—and earn interest directly from people who want to borrow them. This is the simple idea at the heart of earning yield with stablecoins.

A traditional bank would sit in the middle, taking a hefty slice of the profits for its trouble. DeFi protocols, on the other hand, use smart contracts (bits of self-executing code) to handle everything automatically. This efficiency is exactly why stablecoin interest rates can be so much better than what your bank offers. For anyone sitting on cash, it's a powerful new way to put that money to work.

Why Are Stablecoin Yields So Attractive?

The real magic isn't just that the potential returns are higher. It’s that they are generated through a system that’s more transparent, direct, and accessible than the old way of doing things.

Let's quickly compare what you get with DeFi versus a standard savings account.

Stablecoin Interest vs Traditional Savings At A Glance

Feature | Stablecoin Lending (DeFi) | Traditional Savings Account |

|---|---|---|

Typical Yields | Often 5% - 15%+ APY, but can be much higher (and more volatile). | Averages around 0.50% - 2% APY, even for "high-yield" accounts. |

How Yield Is Generated | Interest paid directly by borrowers on-chain; you capture most of the value. | Bank lends out your deposits and pays you a tiny fraction of the profit. |

Access & Speed | Near-instant deposits/withdrawals, 24/7 access, global. | Business hours, 1-3 day transfer times, geographically limited. |

Transparency | All transactions are public on the blockchain. You see the rates in real time. | Opaque. The bank sets the rates and can change them without much notice. |

Control | You typically hold your own keys and control your funds (self-custody). | The bank holds your money. You are a creditor to the bank. |

As you can see, the DeFi approach offers a completely different model. You're not just a customer; you're a direct participant in a financial market.

The core reasons people are flocking to stablecoin yields boil down to a few key points:

Higher Potential Returns: It’s not uncommon to see APYs that blow traditional high-yield savings accounts out of the water.

Direct Market Access: You are literally the bank. You’re earning directly from the demand for capital, cutting out the middleman who would normally skim most of the profit.

Transparency and Control: Every transaction is on a public ledger. You're in charge of your assets, not a faceless institution.

The real shift here is moving from a system where banks tell you what your money is worth to one where open-market supply and demand sets the price in real time. That's the dynamic that unlocks the potential for superior stablecoin interest rates.

This guide will walk you through exactly how these rates are set, what makes them go up or down, and the risks you absolutely must be aware of. Once you get the mechanics, you'll be in a much better position to navigate this space. If you want to dive deeper, you can learn more about how to earn interest on stablecoins in our detailed overview. It’s a new financial frontier, and for those willing to learn, it’s a compelling way to make your money work harder.

How Stablecoin Interest Rates Are Calculated

Unlike your typical bank where rates are decided behind closed doors, stablecoin interest rates in DeFi are set by a dynamic, transparent engine that’s all powered by code. The fuel for this engine is one of the oldest concepts in economics: real-time supply and demand within a specific lending protocol.

Think of it like a massive, automated pawn shop that only deals in digital dollars. On one side, you have lenders (that’s you!) who deposit their stablecoins into a giant pool, making them available for others to use. On the other side, you have borrowers who need cash and are willing to pay a fee—the interest—to get it.

The interest rate is simply the price that keeps these two sides in balance. When lots of people want to borrow but there aren't enough stablecoins to go around, the price to borrow goes up. This higher rate is a signal, tempting more lenders to deposit their funds. On the flip side, if the pool is overflowing with stablecoins and hardly anyone is borrowing, the rate drops to attract more borrowers.

The Utilization Rate: The Key Metric

To make this balancing act happen automatically, DeFi protocols lean on one core metric: the utilization rate. This is the single most important number to grasp if you want to understand how rates are set on platforms like Aave or Compound.

The utilization rate is simply the percentage of all the money in a lending pool that’s currently being borrowed. A high utilization rate means there’s strong demand to borrow, which the protocol’s algorithm uses to push interest rates higher.

For example, say a lending pool holds $100 million in USDC. If $75 million of that is borrowed, the utilization rate is 75%. That's pretty high, and it would translate into an attractive APY for lenders. But if only $10 million were borrowed, the utilization rate would be a sleepy 10%, leading to a much lower interest rate for depositors.

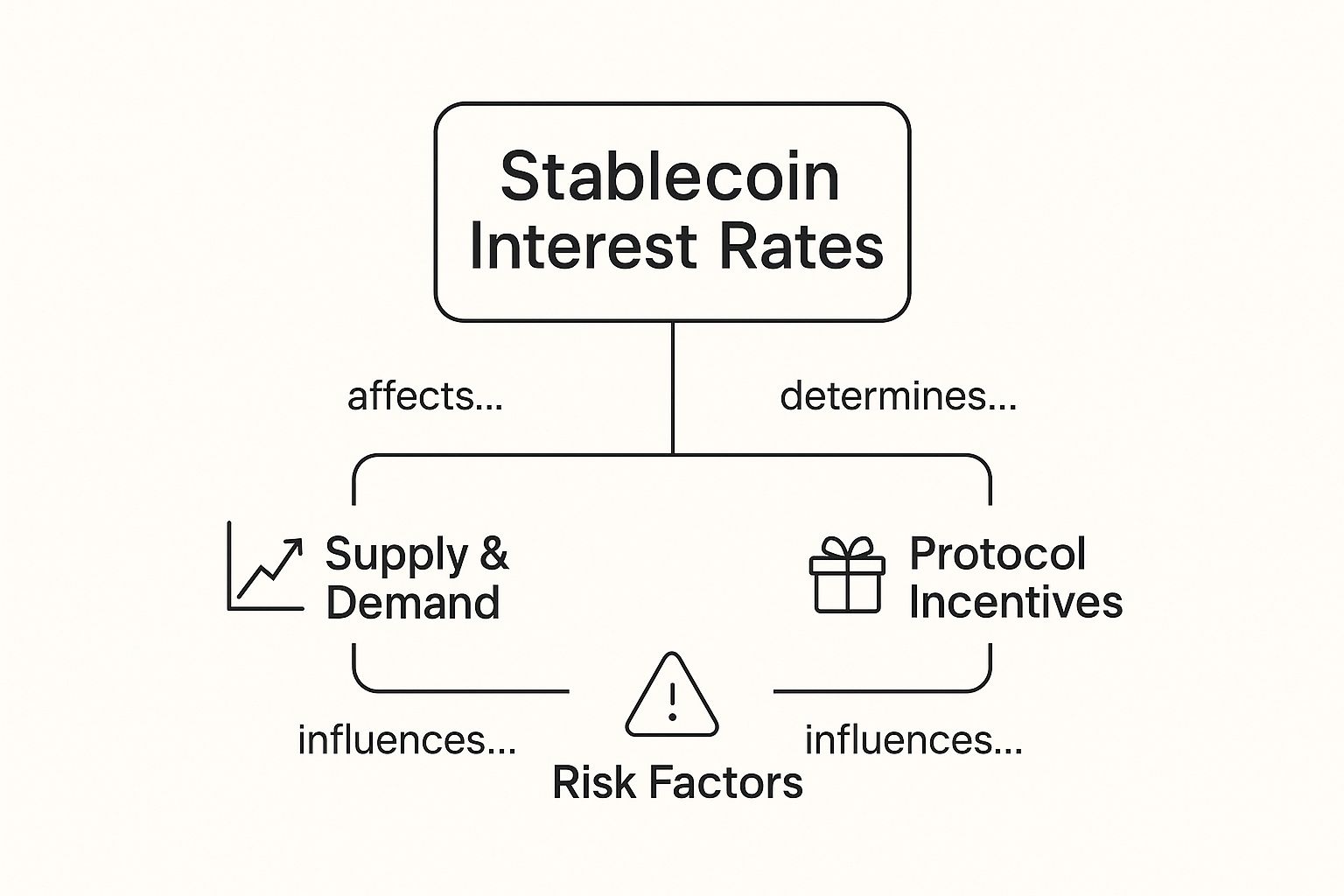

This infographic breaks down how supply, demand, and other forces all feed into the final interest rate you see.

As the diagram shows, while supply and demand are the core engine, things like protocol incentives and external risk factors can also influence whether capital flows in or out, shaking up the rates.

How Algorithms Adjust Rates

Every lending protocol has its own unique algorithm, but most follow a similar pattern. They map out an interest rate curve that ties the utilization rate directly to the APY. This isn't just a straight line; it’s more of a "hockey stick" curve that slopes up gently at first, then shoots up dramatically after hitting a certain point.

Low Utilization (e.g., 0-70%): The interest rate climbs slowly. The goal here is to keep borrowing cheap enough to encourage activity.

High Utilization (e.g., 70-90%): The rate starts to accelerate upwards, much faster. This is a clear signal that the pool is getting tight on funds and needs more deposits from lenders.

Very High Utilization (e.g., 90%+): The rate becomes extremely high. This does two things: it powerfully incentivizes new deposits while making it painfully expensive to borrow, discouraging more withdrawals and keeping enough cash on hand for any lenders who want to pull their money out.

This whole algorithmic dance ensures the lending pool stays healthy and can always meet withdrawal requests. It's a self-correcting system designed to find balance without a human needing to flip a switch.

A Practical Example of Rate Changes

Let's walk through a quick scenario to see this in action.

Stable State: A USDC pool on a DeFi platform has a 50% utilization rate, offering lenders a solid 5% APY. Things are calm.

Demand Spike: Suddenly, a hot new trading opportunity pops up. Traders rush to borrow USDC to get in on the action, pushing the utilization rate up to 85%.

Rate Adjustment: The protocol's algorithm sees the utilization rate jump past its threshold. It automatically jacks up the lender's APY to 12% to attract fresh capital and stabilize the pool.

Capital Inflow: Lenders, including automated strategies from platforms like Yield Seeker, spot the juicy rate and move their capital into the pool. This flood of new USDC brings the utilization rate back down to 75%.

New Equilibrium: With the pressure eased, the algorithm adjusts the APY down to 9%. The market has found a new, higher baseline rate, rewarding lenders for stepping up to meet the increased demand.

This entire cycle can play out in a matter of hours, which is why stablecoin interest rates are so fluid. They're a direct, live-fire reflection of market activity, always adjusting to find that sweet spot between what borrowers will pay and what lenders will accept.

What Factors Influence Your Stablecoin Yield

While the core engine for stablecoin interest rates is simple supply and demand, that's really just the beginning of the story. A few powerful forces, both from the traditional financial world and from within crypto itself, are constantly causing these yields to swing. Getting a handle on them is the key to making smarter decisions and seeing market shifts before they happen.

You can think of these influences in three main layers: the big-picture economic trends, the crypto market's own emotional rollercoaster, and the nitty-gritty details of the specific stablecoin and platform you're using. Each layer adds a new piece to the puzzle of why rates are what they are on any given day.

Macroeconomic Winds and Their Ripple Effects

Believe it or not, DeFi doesn't exist in a bubble. Major trends in traditional finance (TradFi) create powerful currents that inevitably flow into crypto, and they have a direct impact on the yield you can earn on your stablecoins.

The biggest outside influence, by far, is what’s happening with government bonds—specifically, U.S. Treasury yields. In the finance world, these are considered the "risk-free rate." When the return on these super-safe assets goes up, it acts like a magnet for capital from all over.

Think about it: if a U.S. Treasury bill is offering a guaranteed 5%, a DeFi protocol has to offer something better to convince you to take on the extra crypto-related risks. This competition for your money forces stablecoin interest rates to climb just to stay in the game. On the flip side, when Treasury yields drop, DeFi rates have more breathing room to come down while still looking attractive.

And this connection isn't just theoretical. A recent analysis found that large movements of stablecoins—we're talking an average five-day flow of $0.812 billion—have a strong link to changes in the U.S. Treasury yield curve. Looking at over 1,000 data points, the report shows just how intertwined these two worlds have become. You can dig into the full report on how stablecoin flows impact Treasury yields if you want to go deeper.

The Crypto Market Cycle

Anyone who's been in crypto for more than a week knows it runs on cycles of wild excitement and crushing fear. This market sentiment is a massive driver of borrowing demand, which in turn sets interest rates.

Bull Markets (High Demand): During a bull run, everyone feels like a genius. Traders are eager to borrow stablecoins to go long on assets like Bitcoin or Ethereum, hoping to multiply their profits. This massive spike in borrowing pushes demand through the roof, causing stablecoin interest rates to soar.

Bear Markets (Low Demand): When the bear market hits, the party's over. Traders pull back, sell off assets, and run for safety. The desire to borrow stablecoins evaporates, utilization rates on lending platforms crash, and interest rates fall right along with them.

A good way to picture it is to think of a bull market as a gold rush. Everyone is borrowing shovels (stablecoins) to dig for gold (volatile crypto). Naturally, the price to rent a shovel skyrockets. In a bear market, those shovels just sit in a shed, and you can rent one for next to nothing.

Protocol and Asset-Specific Factors

Finally, let's zoom in. Beyond the global economy and the crypto market's mood swings, the specific platform and stablecoin you choose play a huge part in the yield you'll get. Not all yields are the same because not all protocols and assets are trusted equally.

Here are the details that matter most:

Platform Incentives: Many DeFi protocols kickstart their growth with liquidity mining programs. They offer extra token rewards on top of the natural interest rate to attract users and their cash. This can lead to some eye-popping APYs, but be warned—these incentive programs are usually temporary.

Protocol Security: A platform's track record is everything. A protocol that's been audited by reputable firms and has run for years without getting hacked is seen as much safer. Lenders are often happy to take a slightly lower, more reliable yield from a "blue-chip" platform like Aave or Compound over a crazy-high, risky yield from some new, unaudited project.

Stablecoin Reputation: The stablecoin itself is a huge factor. A well-established and transparently backed stablecoin like USDC will have different interest rate behavior than a newer, unproven algorithmic one. A long history of holding its $1 peg builds trust, which attracts more liquidity and leads to more stable—though sometimes lower—interest rates.

Navigating The Risks Of High-Yield Stablecoins

Those juicy stablecoin interest rates can be incredibly tempting, but let's be real—they aren't free money. In any financial world, and especially in DeFi, higher yield almost always means higher risk. Chasing a big APY without understanding the trade-offs is like seeing a shimmering oasis in the desert; it looks fantastic from a distance, but you might find it’s just a mirage.

A smart investor always looks under the hood, past the shiny advertised returns, to see what could go wrong. The good news is that the main dangers in stablecoin lending boil down to three key areas. Getting your head around these is the first step to building a strategy that doesn’t blow up.

Smart Contract Risk: The Flaw in the Digital Blueprint

Every single DeFi protocol runs on a smart contract. This is just self-executing code that manages all the money—the lending, borrowing, and interest payments. Think of it like the blueprint for a high-tech bank vault. If that blueprint is flawless, your money is safe. But if there's one tiny, overlooked error in the code, a clever hacker can find it and walk away with everything inside.

That’s smart contract risk in a nutshell. A bug or a vulnerability in the protocol’s code can be exploited, potentially leading to a total loss of all the funds you’ve deposited. And while the best protocols get multiple security audits from top firms, no code is ever 100% perfect.

Smart contract risk is the most fundamental danger in all of DeFi. You're essentially betting on the quality and security of the code itself. Even the biggest, most trusted platforms have been hacked, which is a stark reminder to never invest more than you can afford to lose.

De-Pegging Risk: When A Dollar Isn't A Dollar

The whole point of a stablecoin is right there in the name—it's supposed to stay stable, pegged to a fiat currency like the U.S. dollar at a $1.00 value. De-pegging risk is the very real danger that a stablecoin breaks that peg and loses its value, which would wipe out your principal and any interest you've earned. This can happen for a few reasons:

Dodgy Reserves: If the assets backing the stablecoin aren't high-quality or can't be sold quickly, a moment of fear can trigger a classic bank run, causing the peg to collapse.

Market-Wide Panic: Big, scary market events can send everyone running for the exits at once. They start dumping their stablecoins, overwhelming the systems designed to keep the price at $1.

We saw a perfect, real-world example of this not too long ago. When Silicon Valley Bank (SVB) went under in early 2023, it sent shockwaves through the crypto market. In March 2023, USDC—one of the biggest stablecoins—saw its market cap drop by almost $10 billion as it briefly de-pegged, falling below 90 cents before it managed to recover. The event was a wake-up call, showing how even the giants are vulnerable to market shocks. If you want to go deeper, the Federal Reserve published a great analysis on how stablecoins react to these crises.

Platform Risk: It's Not Just About the Code

Finally, you have to think about platform risk. This isn’t about a bug in the code; it’s about the people and processes running the show behind the scenes.

This is a broad category that covers everything from bad management decisions and sloppy security to outright scams, like a "rug pull" where the founders just vanish with everyone's money. It also includes operational blunders, like someone losing the private keys that control the protocol, which is like handing a hacker the keys to the kingdom. You have to vet the team's reputation, their transparency, and whether they seem committed for the long haul. That’s just as important as reading a security audit.

To really keep your capital safe, you have to get comfortable with these potential pitfalls. For a more comprehensive look, check out our guide on understanding yield farming risks, which takes an even deeper dive. Being informed is what allows you to make calculated decisions, balancing those attractive stablecoin interest rates with a clear-eyed view of what could go wrong.

Comparing The Top Stablecoins For Yield Generation

When you're chasing yield, it's easy to think a digital dollar is a digital dollar. But that's a mistake. The specific stablecoin you choose—whether it's USDC, USDT, or DAI—is one of the most critical decisions you'll make. This isn't just about picking a favorite brand; it's a calculated choice based on risk, transparency, and rock-solid stability.

You have to look under the hood. What actually backs each stablecoin? The answer to that question directly impacts how safe it's perceived to be, which in turn dictates the stablecoin interest rates it can command across DeFi. Getting a handle on these fundamentals is the key to making a smart choice based on your own risk appetite, not just blindly chasing the highest number you see.

Fiat-Collateralized vs. Crypto-Collateralized

Let’s get right to it. The most common stablecoins are split into two major camps based on how they hold their value. This is the first and most important difference to wrap your head around.

Fiat-Collateralized (like USDC and USDT): These are the most direct. For every single token out there, the company behind it holds an equivalent amount of real-world assets in the bank. Think of it as a vault filled with cash and super-safe government bonds. Their stability is only as good as the quality and transparency of those reserves.

Crypto-Collateralized (like DAI): This is where things get a bit more "crypto-native." These stablecoins are backed by other cryptocurrencies. To mint DAI, for instance, a user has to lock up a larger value of a more volatile coin like Ethereum into a smart contract. This "over-collateralization" creates a safety cushion to absorb price shocks.

For most folks just getting their feet wet with yield farming, fiat-backed coins are the go-to. Their connection to traditional, verifiable assets gives them a much clearer and more trusted foundation.

Key Takeaway: A stablecoin is only as strong as its reserves. One backed by cash and boring old government debt is generally a much safer bet than one propped up by volatile crypto assets.

A Closer Look at The Market Leaders

Okay, let's break down the big three you'll see everywhere. Each one has its own personality, which affects how it fits into your yield strategy.

USDC (USD Coin): Most people see USDC as the gold standard for playing by the rules. It's issued by Circle and is backed entirely by cash and short-term U.S. government debt. They're big on regular audits and a conservative approach, making it the top pick for anyone who puts safety first.

USDT (Tether): This is the behemoth. USDT is the largest stablecoin by a country mile and the lifeblood of crypto trading. While it’s faced some tough questions about its reserves in the past, Tether has gotten much better at showing its work. Because it’s so liquid and in high demand, it often pulls in some very competitive stablecoin interest rates.

DAI: This is the OG decentralized, crypto-backed stablecoin. It’s not run by a company but by the MakerDAO community. Its peg is held steady by a complex dance of smart contracts and collateralized loans. It’s definitely more complex, but its decentralized ethos is a huge draw for people who’d rather not trust a central corporation.

The track record of these assets is a huge tell. Research looking at stablecoin performance from mid-2021 to mid-2023 found that while both USDC and USDT held their peg tightly, other stablecoins saw much bigger price wobbles. Those fluctuations are poison for yield because lending protocols need unwavering stability to function. For a deeper dive, you can check out S&P Global's report on stablecoin price stability and market trust.

At the end of the day, the "best" stablecoin is the one that fits your personal goals. For those looking to automate their strategy and squeeze every last drop of yield out of the market, knowing these differences is just the start. To see how to put these assets into action, check out our complete guide on stablecoin yield farming.

Alright, theory's great, but making real money from your stablecoins is what actually matters. The trick is to stop just parking your funds and start actively managing them to chase down the best yields—all while keeping a close eye on risk. It's about shifting from a passive holder to an active earner.

Let’s get into three core strategies to get you there: yield farming, using yield aggregators, and the golden rule of diversification. Each has its place in building a smart, effective plan for your stablecoins.

Actively Pursue Higher Yields

The most hands-on way to do this is called yield farming. Honestly, it’s a bit like being a relentless bargain hunter. You're constantly on the lookout for the best deals in DeFi, which means moving your stablecoins between different lending protocols to grab the highest APYs as they pop up.

For instance, maybe Aave is offering a respectable 7% on USDC. But then you spot a newer, audited protocol offering 11% because of a short-term spike in borrowing demand. A savvy yield farmer would jump on that, move their funds, and capture that higher rate. It takes work, constant monitoring, and paying some gas fees, but for those willing to do it, the boost in returns can be significant.

Automate Your Strategy With Yield Aggregators

If manually chasing rates sounds like a full-time job you don't want, then yield aggregators are going to be your new best friend. Think of them as the robo-advisors of DeFi. You just deposit your stablecoins, and the platform does all the heavy lifting—finding the best returns and compounding them for you automatically.

Yield aggregators are game-changers because they automate the entire, often complicated, process of yield farming. They scan the market 24/7, shuffle funds to the most profitable spots, and reinvest your earnings. They turn a seriously labor-intensive task into a passive income stream.

Platforms like Yield Seeker are a perfect example of this in action. By using an AI agent, it can analyze opportunities across tons of protocols in real-time, pulling off a strategy that would be almost impossible for a human to manage alone. This doesn't just save you a massive amount of time; it uses technology to squeeze every last drop of potential out of your stablecoin interest rates, day and night.

Diversify Everything To Manage Risk

This one is non-negotiable. Seriously. While chasing juicy yields is exciting, protecting your capital is always priority number one. Diversification is your best defense against all the weird and unexpected things that can happen in crypto. Smart diversification isn’t just about one thing, either—it happens on a few different levels:

Across Different Stablecoins: Don't bet the farm on a single stablecoin. Holding a mix of top-tier stables like USDC and USDT can save you a lot of grief if one of them has a bad day and temporarily de-pegs.

Across Different Platforms: Spread your capital across a few well-known, audited lending protocols like Aave and Compound. This contains the damage if one platform gets hacked or runs into a critical bug. Your whole stack won't be at risk.

Across Different Blockchains: For the more advanced folks, consider putting your assets to work on different blockchains (like Ethereum, Base, or Solana). This protects you from chain-specific problems, like a sudden spike in gas fees on one network or a temporary outage.

When you blend these strategies—actively hunting for yield, automating the grunt work, and diversifying like your life depends on it—you build a really balanced approach. You get to chase those high returns with confidence, knowing you've built a resilient portfolio that can handle the inevitable market bumps. That’s how you graduate from being a passive holder to a strategic earner in DeFi.

Dipping your toes into the world of stablecoin yields always brings up a few questions. It’s only natural. Before you put any real capital to work, you want clear, straight-to-the-point answers. Let’s tackle some of the most common things people ask so you can move forward with confidence.

Is Earning Interest On Stablecoins Safe?

It’s definitely seen as a tamer activity than, say, speculating on Bitcoin or Ethereum, but earning interest on stablecoins is not risk-free. Anyone who tells you otherwise isn't giving you the full picture.

You're mainly looking at a few potential tripwires: bugs in a platform's smart contract code, the ever-present threat of a platform hack, and the small but real chance that a stablecoin could lose its one-to-one peg to the dollar.

So, how do you protect yourself? Stick to reputable, well-audited DeFi platforms and don't put all your eggs in one basket. Spreading your funds across different stablecoins and protocols is just smart practice. And always remember, this isn't your neighborhood bank—your funds aren't covered by government protections like FDIC insurance.

Do I Have To Pay Taxes On Stablecoin Interest?

Yes, almost certainly. In most places, including the United States, the interest you earn from lending out your stablecoins is considered taxable income. The exact rules and how much you’ll owe can get complicated, changing based on where you live and your own financial situation.

The world of digital asset taxes is still a bit of a maze and the rules are constantly being updated. Your best bet is to talk to a qualified tax professional who knows the crypto space. They can give you advice that actually applies to you and make sure you’re playing by the rules.

If there's one thing to take away, it's that regulators are starting to look at stablecoin activity just like they look at traditional finance. Thinking of your earnings as regular income is the safest way to stay on the right side of the law.

Why Do Stablecoin Interest Rates Change So Often?

That constant movement in stablecoin interest rates is a core feature of DeFi, not a bug. These rates aren't decided in a boardroom; they're the direct result of real-time supply and demand playing out in decentralized lending pools.

When a lot of people want to borrow, the protocol’s algorithm automatically bumps up the APY. Why? To tempt more lenders (like you) to deposit their capital. On the flip side, if the pool is flush with cash and not enough people are borrowing, rates will drop to make borrowing more attractive. This all happens on the fly, which is why the APY can bounce around, sometimes even hour by hour.

What Is The Difference Between APY and APR?

Getting this one right is key to figuring out what you’ll actually earn. They sound similar, but they tell you very different things.

APR (Annual Percentage Rate) is the simple, no-frills interest rate. It's what you'd earn over a year without any compounding.

APY (Annual Percentage Yield) is the one you really want to watch. It accounts for the magic of compounding—that's when your interest starts earning its own interest.

Since most DeFi protocols are set up to automatically compound your earnings (often many times a day), APY gives you a far more accurate picture of your total potential returns over a year.

Stop wasting time chasing yields and let artificial intelligence do the work for you. Yield Seeker uses a sophisticated AI Agent to scan the market 24/7, automatically moving your funds to the highest-yielding opportunities on the BASE chain. Start earning smarter, not harder. Explore how it works at https://yieldseeker.xyz.