Back to Blog

What Is Annual Percentage Yield and How Does It Work?

What is annual percentage yield (APY)? Learn how APY works, how to calculate it, and how compounding interest helps you maximize your savings.

Aug 7, 2025

published

Let's get right to it. Annual Percentage Yield (APY) is the real return you earn on your savings over a year, all thanks to the power of compounding interest.

Imagine a snowball rolling downhill. It doesn't just grow from the fresh snow it picks up; it also grows from the snow already stuck to it. This makes it get bigger and bigger, faster and faster. That's exactly how your money works with APY.

Decoding Your Money’s Growth Engine

Even if the term sounds a bit technical, APY is your most accurate tool for seeing your money's true growth potential. Whether you're looking at a high-yield savings account, a certificate of deposit (CD), or even a crypto account that earns interest, APY gives you the full picture. It goes beyond a simple interest rate to show what you'll actually have in your account after a year, because it factors in compounding.

Compounding is where the magic happens. It’s the process of earning interest not just on your initial deposit (the principal) but also on the interest you've already earned. This is what creates that accelerating growth curve, turning APY into an essential number for any savvy saver.

Core Components of Your Annual Percentage Yield

To really get a handle on what annual percentage yield is, it helps to see it as a combination of a few key parts. Each piece plays a specific role in calculating your final return.

This table breaks down the fundamental elements that determine the final APY on your savings account.

Component | What It Means for You | Impact on Your APY |

|---|---|---|

Principal | The initial amount of money you deposit. Your starting capital. | The larger your principal, the more interest you earn in dollar terms, even if the rate is the same. |

Interest Rate | The base percentage your money earns, set by the financial institution. | This is the foundation of your earnings, but it doesn't tell the whole story without compounding. |

Compounding Frequency | How often interest is calculated and added back to your balance. | More frequent compounding (e.g., daily vs. annually) leads to a higher APY and faster growth. |

Thinking about these components helps you understand why one account might be a better choice than another, even if their base rates look similar.

The most important thing to remember is this: APY gives you a standard, apples-to-apples way to compare different savings products. A higher APY means more money in your pocket over time. It's the single best tool for deciding where to put your savings to work.

How To Calculate Your APY and See the Growth

While it's great to know what APY is, seeing how the sausage is made is what really brings its power to life. You definitely don’t need a math degree to get a handle on it; the formula is just a simple way to visualize how compounding interest works its magic over a year.

The standard formula you'll see is: APY = (1 + r/n)^n - 1

Let's break that down into plain English:

r: This is your starting interest rate, the one advertised upfront. Think of it as the base rate.

n: This is the key ingredient—the number of times your interest gets paid out (compounded) each year.

That little "n" is where the magic happens. It represents how frequently your earnings are rolled back into your principal, which then starts earning interest of its own. This is exactly why a higher compounding frequency leads to a better APY, even if two accounts share the same base interest rate.

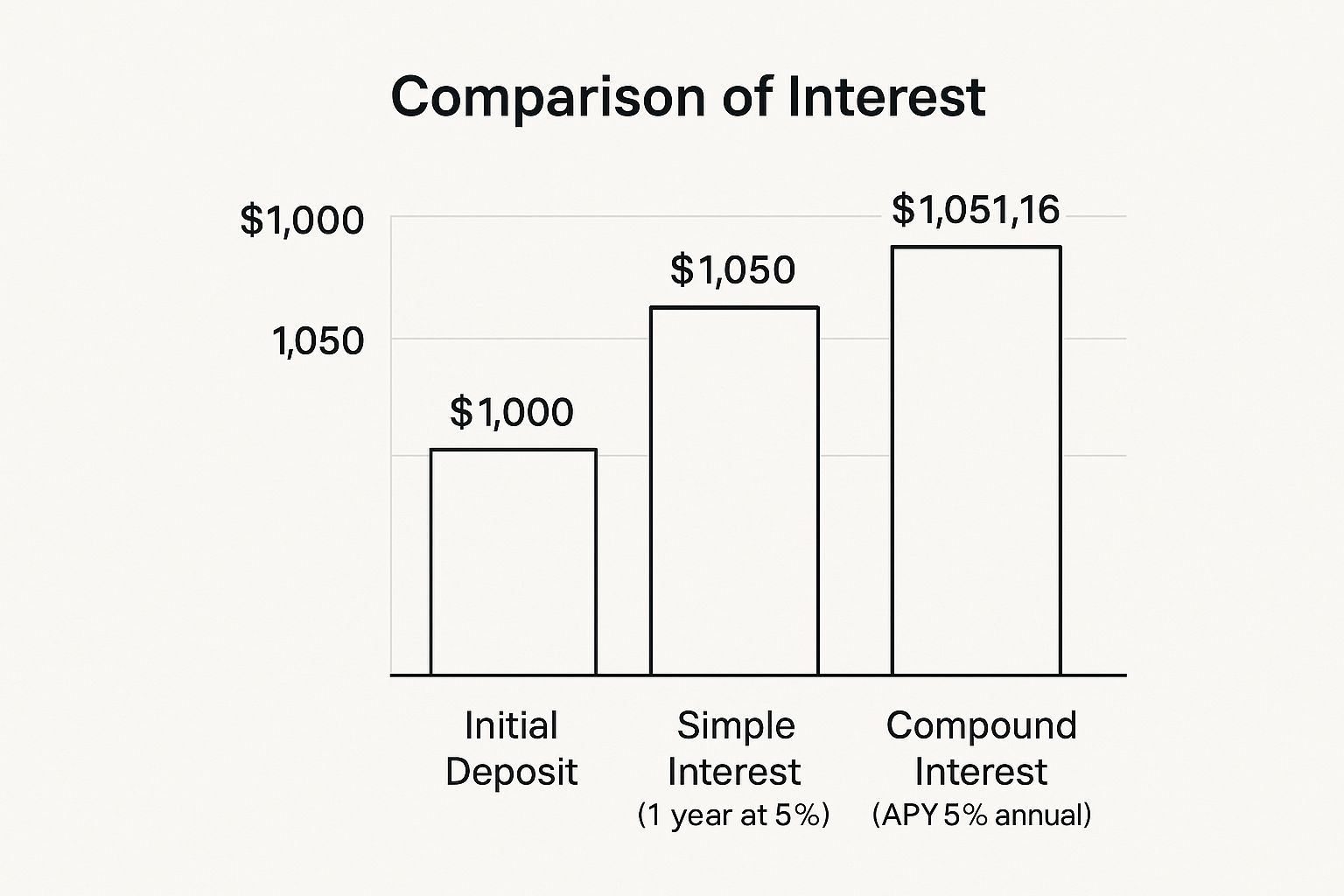

A Real-World Calculation Example

Let's walk through a practical scenario. Imagine you put $1,000 into an account that offers a 5% annual interest rate. We'll look at how your earnings change based on whether the interest is compounded monthly or daily.

Scenario 1: Compounded Monthly (n=12)

APY = (1 + 0.05/12)^12 - 1

APY ≈ 5.116%

Your Balance After One Year: $1,051.16

Scenario 2: Compounded Daily (n=365)

APY = (1 + 0.05/365)^365 - 1

APY ≈ 5.127%

Your Balance After One Year: $1,051.27

You can see that daily compounding gives you a slightly higher APY and, consequently, a little more cash in your pocket. While the difference on $1,000 might not seem huge, this effect snowballs with larger sums and over longer timeframes.

Once you get a feel for this formula, you can start looking past the advertised rates and see the true growth potential of an investment. It gives you the power to compare different offers on an apples-to-apples basis and pick the one that will actually make your money work hardest for you.

If you'd rather not do the math by hand, there are plenty of free online tools that can crunch the numbers for you. For a more detailed walkthrough, be sure to check out our complete guide on how to calculate APY for any type of investment. It's a fundamental skill for making smart financial choices.

Understanding The Difference Between APY And APR

APY and Annual Percentage Rate (APR) sound incredibly similar, but in the world of finance, they're practically polar opposites. Getting a handle on this difference isn't just a technicality—it's essential for making smart decisions with your money, because one tells you what you earn, and the other tells you what you pay.

Here’s a simple way to think about it: APY is your 'growth engine' for savings and investments. It reveals the true return you can expect after a year. On the other hand, APR is the 'cost meter' on any money you borrow, showing the total price you'll pay annually for that loan. Naturally, you want the highest APY possible on your savings and the lowest APR on any debt.

The magic ingredient in APY is compounding. The infographic below shows just how powerful this effect can be, even with small amounts. It’s the difference between earning interest on your initial deposit versus earning interest on your deposit and the interest it's already generated.

That little extra boost from compounding is what makes APY the more accurate measure of growth. It’s your money working harder for you.

To make this crystal clear, let's break down when to focus on each metric. Here's a quick comparison to start.

APY vs APR: A Quick Comparison

Feature | Annual Percentage Yield (APY) | Annual Percentage Rate (APR) |

|---|---|---|

What It Measures | The total return on an investment over a year. | The total cost of borrowing money over a year. |

Includes Compounding? | Yes. It accounts for interest earned on interest. | No. It's a simple interest rate plus fees. |

You Want It To Be... | High. A higher APY means more earnings. | Low. A lower APR means less cost to you. |

Primary Use | Savings accounts, CDs, crypto staking, yield farming. | Credit cards, mortgages, auto loans, personal loans. |

This table lays out the core distinction: APY helps you grow your wealth, while APR helps you manage the cost of debt.

When APY Is Your Best Friend

Anytime you're saving or investing, APY is the number you should care about most. Because it includes the effects of compounding, it gives you the most honest picture of your potential earnings. Whether you're comparing high-yield savings accounts, Certificates of Deposit (CDs), or DeFi strategies like those offered by Yield Seeker, the higher APY will always put more money in your pocket, all else being equal.

When To Focus On APR

Conversely, your focus should flip to APR the moment you consider borrowing money. APR represents the simple interest rate plus any fees the lender rolls into the loan, like origination or processing fees. This makes it the single best metric for comparing the true cost of things like:

Credit Cards: The APR shows how much interest racks up on any balance you carry over.

Mortgages and Auto Loans: It gives a much fuller picture of your borrowing costs than the headline interest rate alone.

Personal Loans: Comparing APRs is the fastest way to find the most affordable loan.

The key takeaway is that APR typically doesn't account for compounding against you in the same way APY accounts for it for you.

A simple rule of thumb: When you're the one earning money, look for the highest APY. When you're the one paying money, hunt for the lowest APR.

Keeping this distinction straight is fundamental to good financial health. It helps you make smarter choices, whether you’re trying to build your wealth or just manage your expenses.

How Economic Shifts Affect Your Savings Growth

Have you ever looked at the return on a savings account and wondered why it’s so much lower than what your parents or grandparents used to get? It’s a common question, and the answer isn't that banks are just getting stingier. The annual percentage yield (APY) you earn is directly tied to the bigger economic picture.

Think of it this way: central banks, like the Federal Reserve in the U.S., act as the economy's thermostat. When inflation gets too hot, they raise interest rates to cool things down. This move makes it more expensive for banks to borrow money, and they, in turn, offer you a higher APY on savings to attract your cash. For savers, this is great news.

On the flip side, when the economy is sluggish, central banks lower rates to encourage people and businesses to borrow and spend. While this can help stimulate growth, it means the APY offered on your savings accounts and CDs will drop, sometimes significantly.

A Look at Historical APY Trends

This isn't just theory; you can see it clearly by looking back at historical rates. During the high-inflation era of the 1980s, it was possible to find a one-year CD with an APY above 11%. That’s almost unthinkable today.

But after the 2008 financial crisis, the Fed slashed rates to near zero, and for years, most savings accounts paid less than 1%. More recently, in the fight against post-pandemic inflation, rates climbed again. By 2023, you could find one-year CDs offering around 4.40%, the best returns savers had seen in over 15 years. You can see a great breakdown of these fluctuations in CD rates on Bankrate.com.

Understanding this relationship is key. It reframes APY from a simple, static number into a dynamic indicator of the economy's health. With this insight, you can make more informed choices about when to lock in a high-yield CD or when to look for other ways to grow your money.

For those who want to find strong returns no matter which way the economic winds are blowing, it's worth exploring alternatives to traditional banking. To see what's possible, check out our guide on finding the highest APY in yield farming.

Why Global Trends Also Shape Your APY

Ever wonder why the APY on your savings account seems to have a mind of its own? It’s not just your bank making a random decision. In reality, that rate is deeply connected to huge economic forces playing out across the globe.

Think of it like this: your local bank is a small boat, but it's floating on a massive ocean. The tides and currents of that ocean—global economic trends—have a much bigger say in where your boat ends up than your own paddling does.

The Ripple Effect from Government Bonds

One of the most powerful currents in finance is the yield on government bonds. When major economies like the United States, Germany, or Japan issue bonds, the interest they promise to pay acts as a baseline for a "risk-free" investment. Everyone, from big financial institutions to your local bank, pays close attention.

If the U.S. government is offering a 3% return on its bonds, your bank knows it has to offer an APY that's at least competitive. Why? Because they need to give you a good reason to park your cash with them instead of in a super-safe government bond.

Putting Your APY in a Global Context

This connection is why a 2% APY can feel amazing one year and completely underwhelming the next. It’s all about the bigger picture. Historically, long-term government bond yields in major developed markets have often floated between 2% and 4%. You can see how these global bond rates have trended over time on the St. Louis Fed's website. When those yields go up, bank APYs tend to follow. When they fall, APYs get dragged down with them.

This means your APY isn't just an isolated number. It's a direct reaction to international monetary policy, inflation, and the overall stability of the global financial system.

Grasping this link is key. It helps you understand the true value of your returns and pushes you to look for opportunities that can thrive even when traditional markets are sluggish. For example, exploring the best stablecoin yields offers a chance to earn returns that often operate outside the direct influence of traditional banking and government policies.

Your Top APY Questions, Answered

Once you get the hang of what APY is, you'll naturally start thinking about how it works in the real world. Let’s walk through some of the most common questions that pop up. Answering these will help you feel more confident when putting your money to work.

Is a Higher APY Always the Best Choice?

In a perfect world, yes. A higher APY means your money grows faster. But the real world is rarely that simple.

That amazing APY you see advertised might come with strings attached. Be on the lookout for hidden monthly fees, strict minimum balance requirements, or limits on how often you can withdraw your money. These little details can quickly chip away at your earnings.

The lesson here is to always read the fine print. An account with a slightly lower APY but zero fees could easily be the smarter choice in the long run, especially if you can't meet the conditions to waive the fees on the high-yield account.

How Often Does APY Change?

This all comes down to whether your account has a fixed or variable rate.

Fixed APY: This rate is locked in for a set period. Think of a Certificate of Deposit (CD). Your earnings are predictable because the rate won't budge.

Variable APY: This rate can and will change over time. It’s the standard for high-yield savings accounts and DeFi protocols, often moving in response to bigger economic shifts, like when central banks adjust their policies.

What’s Considered a “Good” APY Right Now?

There’s no single answer to this because a "good" APY is a moving target. It’s directly tied to what's happening in the global economy, like inflation and central bank decisions.

For example, in mid-2025, the Bank of England set its base rate at 4.25% to combat inflation, while the European Central Bank’s was 2.15%. This shows how different economic environments lead to different rate expectations. You can dig deeper into these global interest rate trends and their impact on savers to see how they connect.

At the end of the day, a good APY is one that beats inflation, fits your financial goals, and isn’t secretly being eaten by fees.

Ready to stop worrying about fluctuating rates and put your stablecoins to work? Yield Seeker uses an AI-powered agent to automatically find and secure the best yields for you, 24/7. Start earning more with just a $25 deposit at https://yieldseeker.xyz.