You probably have a stablecoin balance sitting in a wallet right now. It might be dry powder for the next market move, operating cash for a team, or money you moved on-chain because transfers are fast and settlement is clean. The question is the same either way: should that balance stay idle, should it be put to work earning yield, or should it support a borrowing strategy?

That decision matters because borrowing isn't some niche corner of finance. It's one of the main ways people and businesses manage cash flow. In the United States, total household debt reached $18.8 trillion at the end of 2025, up $4.6 trillion since 2019, which shows how integral borrowing is to everyday financial life, from homes to education to short-term liquidity needs, as tracked by the New York Fed household debt data.

On-chain, the same logic applies. A stablecoin isn't just digital cash. It's also potential collateral, liquidity, and optionality. Used well, borrowing can help you avoid selling assets, bridge timing gaps, or increase capital efficiency. Used poorly, it can turn a calm portfolio into a liquidation problem you have to babysit.

Rethinking Your Stablecoins From Static Cash to a Dynamic Asset

A lot of people treat stablecoins like a parked car. Safe, useful, and waiting for the next trip. That works if your only goal is preservation. But once you move funds on-chain, that balance becomes more than a placeholder.

Stablecoins can do at least three jobs. They can sit as reserve capital. They can earn yield. Or they can support borrowing, either directly as the asset you borrow or indirectly as the collateral and liquidity base around a larger strategy.

Borrowing is a tool, not a distress signal

In consumer finance, people borrow for all kinds of reasons that have nothing to do with panic. Businesses borrow to smooth cash flow. Homeowners borrow against equity instead of selling their house. Investors borrow because timing matters.

That mindset helps in DeFi. Borrowing doesn't automatically mean you're overextended. Sometimes it means you're trying to keep exposure to an asset while still getting spendable dollars. Sometimes it means you want flexibility without unwinding a position.

Borrowing is most useful when you know exactly what problem it's solving. Liquidity, leverage, or time. If you can't name the job, don't take the loan.

The practical question stablecoin holders face

If you hold USDC or another stablecoin, your real choice isn't just “borrow or don't borrow.” It's closer to this:

Keep funds idle if you need immediate access and don't want protocol risk.

Earn yield if your priority is compounding with less day-to-day management.

Use borrowing if you need liquidity or want to keep another position intact.

The mistake is treating all three as interchangeable. They aren't. Borrowing asks for more attention than passive earning. It introduces moving parts like collateral health, variable rates, and liquidation thresholds. In return, it gives you flexibility that simple yield strategies don't.

A better starting point

Think of stablecoins as a balance sheet item, not just a token balance. Ask two direct questions:

Do I need cash flow, or am I trying to grow idle capital?

Can I monitor a position if markets move fast?

If your answer to the first is “cash flow,” borrowing may belong on the table. If your answer to the second is “not really,” earning may be the better default.

The Universal Mechanics of Borrowing

Borrowing looks more complicated than it is. Strip away the interfaces, legal documents, and crypto jargon, and the core structure stays the same. Someone gives you money now. You promise to give back the principal plus interest later. The lender wants protection in case you don't.

That protection often comes from collateral. The easiest analogy is a home equity line of credit. If a home is worth more than the mortgage against it, the owner has equity. A bank may lend against part of that equity because the house gives the bank a fallback if the borrower defaults.

Collateral, principal, and interest

A few terms do most of the work:

Principal means the amount you borrow.

Interest is the price you pay for using that money.

Collateral is the asset pledged to secure the loan.

If you borrow against a house, the house matters because it reduces lender risk. If you borrow against crypto, the same principle applies. The lender isn't lending on faith alone. They're lending because they can claim or sell the collateral if things go wrong.

In traditional consumer finance, borrowing is common and often practical. In the United States, personal loan debt hit a record $276 billion in Q4 2025, and 51.4% of borrowers used personal loans to consolidate debt or refinance credit cards, according to LendingTree's personal loan statistics. That tells you something important. People don't borrow only to spend more. They also borrow to reorganize obligations.

Loan-to-value in plain English

The key ratio is loan-to-value, often shortened to LTV. It answers one question: how much are you borrowing relative to the value of what you've pledged?

If a lender lets you borrow a conservative amount against collateral, they leave room for price changes, fees, and the messy reality of selling that collateral if needed. If they lend too much, a small drop in collateral value can put the whole loan at risk.

A useful way to think about LTV:

Term | Plain meaning | Why it matters |

|---|---|---|

Low LTV | You're borrowing a smaller amount against collateral | More safety cushion |

High LTV | You're borrowing closer to the asset's full value | Less room for error |

Interest rate | Ongoing cost of the loan | Affects whether the strategy makes sense |

A cautious borrower usually cares less about the maximum available loan and more about the survival buffer.

Practical rule: Borrow based on the worst week you can tolerate, not the best rate you can get.

The mechanics get clearer when you see them in motion:

What confuses people most

People often mix up access to borrowing with capacity to repay. A lender may approve a large amount because the collateral supports it. That doesn't mean the loan fits your plan.

Before you borrow, answer three simple questions:

What asset am I risking?

What happens if its value drops quickly?

What exactly will I do with the borrowed funds?

If you can't answer the third question in one sentence, you probably shouldn't take the loan.

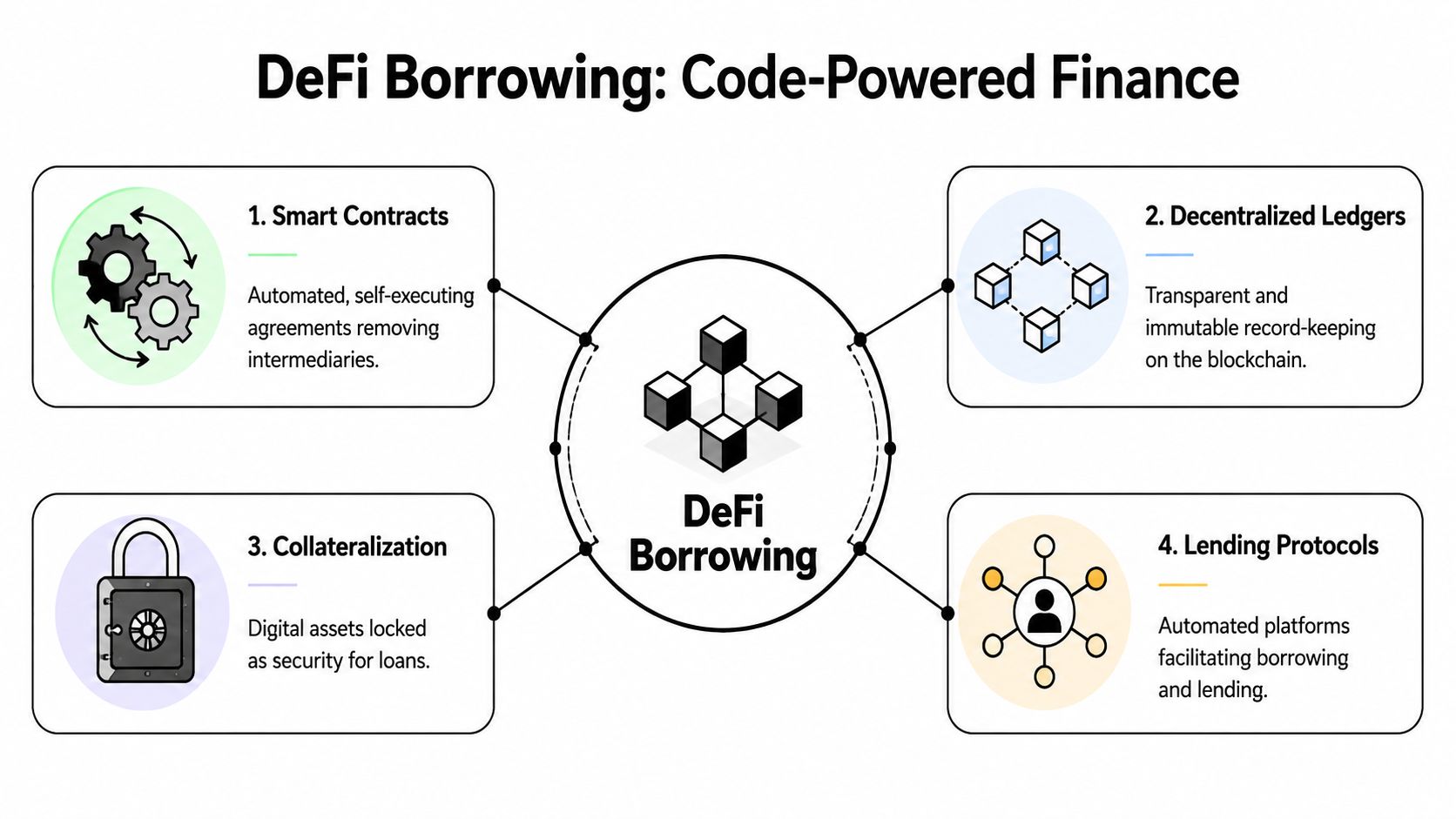

How DeFi Rebuilds Borrowing with Code

DeFi didn't invent borrowing. It rebuilt it so software handles the parts that banks and brokers usually manage. Instead of a loan officer, you interact with a smart contract. Instead of a bank balance sheet, you tap into a liquidity pool. Instead of a manual appraisal, the system relies on external price feeds called oracles.

That shift changes who can participate and how fast the system operates. In traditional lending, access often depends on identity, geography, account history, and underwriting. In DeFi, code checks whether you've posted enough collateral and whether the protocol rules permit the transaction. If yes, the loan can happen.

What replaces the bank

Four moving parts do the heavy lifting on-chain:

Smart contracts enforce the rules automatically.

Liquidity pools hold lendable assets supplied by other users.

Oracles feed in market prices used to value collateral.

Liquidation mechanisms close or reduce risky positions when collateral falls too far.

This is why DeFi borrowing feels immediate. You're not asking a person for permission. You're satisfying a machine-readable set of conditions.

A good mental model is that a DeFi protocol is a public lending engine. Anyone can inspect the rules. Anyone can see the pool. Anyone who meets the conditions can use it.

Why this matters beyond crypto natives

Access is the bigger story. The traditional system still leaves many people out. At the same time, on-chain capital keeps growing. An estimated 1 billion people remain unbanked globally, while DeFi lending protocols like Aave and Compound on Base saw over $10B in stablecoin borrows in Q1 2026, which points to a meaningful opening for blockchain-native credit, as noted in this discussion of underserved markets and DeFi borrowing.

That doesn't mean DeFi has solved credit. Far from it. Most borrowing today is still overcollateralized, which means you usually need to lock more value than you borrow. If you want a clear primer on why that model dominates, this short guide to overcollateralized borrowing is worth reading.

The philosophical shift

Traditional finance asks, “Who are you, and should we trust you?”

DeFi often asks, “What collateral have you posted, and does the code approve the position?”

That sounds simple because it is simple at one layer. But simplicity at the access layer pushes complexity somewhere else. The system no longer depends as much on human judgment. It depends on code quality, collateral design, and market data.

DeFi makes borrowing more open. It doesn't make it less real. The debt still exists, the collateral is still at risk, and the market can still punish bad positioning.

For a stablecoin holder, the key takeaway is that DeFi borrowing is less about paperwork and more about mechanics. If you understand the mechanics, you can make clean decisions. If you don't, the smooth interface can trick you into taking risk you haven't priced in.

A Tour of Common On-Chain Borrowing Products

“Borrowing in DeFi” sounds like one thing. It isn't. Different products exist for different jobs, and confusion usually starts when someone uses the right tool for the wrong reason.

Pooled borrowing for liquidity

This is the format most stablecoin holders will encounter first. Protocols like Aave and Compound let users deposit collateral into a system and borrow against it from shared liquidity pools.

Typical use case: you hold ETH, don't want to sell it, but need USDC for another purpose.

What makes this product attractive is clarity. Deposit collateral, see the borrow capacity, take the loan, monitor the health factor. It's usually the closest on-chain equivalent to a collateralized credit line.

Margin borrowing for trading exposure

Margin products are different. Here, borrowing isn't mainly about liquidity. It's about increasing market exposure.

A trader might post collateral and borrow additional assets to enlarge a long or short position on a decentralized trading venue. The goal isn't cash management. It's amplified returns if the trade works.

That also means the risk is sharper. Borrowing costs matter, but price movement matters more. If you're wrong, losses compound faster because the borrowed capital magnifies the move against you.

Flash loans for developers and power users

Flash loans confuse newer users because they don't behave like normal loans. They're borrowed and repaid in the same blockchain transaction. If the full sequence doesn't complete, the whole transaction reverts.

That makes flash loans useful for:

Arbitrage execution across multiple venues

Collateral swaps that restructure a position

Refinancing flows between protocols without holding idle capital

They are not for ordinary household-style borrowing. They are transaction tools, not ongoing debt products.

Which product fits which person

A quick comparison helps:

Product type | Best for | Main risk |

|---|---|---|

Pooled borrowing | Accessing liquidity without selling assets | Liquidation from collateral decline |

Margin borrowing | Increasing trade exposure | Faster losses from leverage |

Flash loans | Developers and advanced execution flows | Transaction complexity and implementation mistakes |

The important part isn't memorizing product names. It's matching the product to the problem. If you need stable liquidity, don't reach for a margin tool. If you're trying to automate a complex rebalance, a standard loan may be clumsy.

Most mistakes in DeFi borrowing aren't technical. They're category errors.

Navigating the Inescapable Risks of DeFi Borrowing

The appeal of DeFi borrowing is speed and access. The cost is that the system enforces risk with very little sympathy. There is no collections officer calling to work out a payment plan. The protocol checks the numbers, and if the position fails, liquidation logic takes over.

Liquidation risk is the one you feel first

If you borrow against a volatile asset, your biggest operational risk is a falling collateral price. DeFi doesn't wait for a committee meeting. It reacts automatically.

Borrowing becomes precarious when conditions tighten. In traditional markets, a 100 basis-point tightening in financial conditions can significantly stress heavily indebted borrowers, according to the Federal Reserve's discussion of business debt vulnerabilities. On-chain, the same pressure can hit faster because liquidation systems are automated and market moves can feed on themselves.

A borrower often says, “I'm safe because my collateral is strong.” That's only partly true. Strong collateral can still become weak collateral if the market drops quickly enough.

Smart contract risk is infrastructure risk

A DeFi lending protocol is software that holds assets and enforces rules. If the code has a flaw, the protocol can fail even when your market view is correct.

A simple analogy helps. A vending machine is supposed to exchange money for snacks. If someone finds a bug that lets them empty the machine, the problem isn't your snack preference. The machine itself was insecure.

When you borrow through a protocol, you're also trusting:

The contract logic to behave as intended

Upgrade mechanisms not to introduce new vulnerabilities

Administrative controls not to be abused or compromised

Oracle risk sits in the middle

The protocol needs a price to know whether your collateral still supports the loan. If the oracle feed is wrong, stale, or manipulated, the system can make a bad decision based on bad input.

That can trigger unfair liquidations or blocked borrowing capacity. It feels abstract until it happens. Then it becomes the most concrete risk in the stack.

Bad price data can liquidate a good position. That isn't a theoretical edge case. It's a design dependency.

A simple safety checklist

Before opening any on-chain borrowing position, check for these:

Collateral volatility. If the collateral can swing hard, leave more room than you think you need.

Protocol maturity. New systems may offer attractive terms, but less battle-tested code.

Oracle design. Understand where the protocol gets prices and how sensitive your position is to short-lived dislocations.

Monitoring burden. If you won't watch the position, you need a wider margin of safety.

If you want a more structured framework, this guide to mastering on-chain risk management is a strong follow-up.

Healthy skepticism isn't bearish. It's how responsible borrowing works.

Practical Borrowing Strategies for Stablecoin Holders

The cleanest way to understand borrowing is to look at real decision patterns. Not spreadsheets. Not protocol dashboards. Just the situations people face.

The investor who wants exposure without selling

Maya holds ETH and thinks the long-term case is intact. She also wants stablecoins available for another opportunity. Selling the ETH would solve the liquidity problem, but it would also reduce the position she wants to keep.

So she borrows against the ETH instead. The loan gives her spendable stablecoins while preserving market exposure. This is useful when the goal is continuity, not exit.

The catch is obvious. If ETH drops hard, her collateral health worsens. This strategy only works if she keeps a meaningful buffer and understands that borrowed liquidity isn't free liquidity.

The freelancer bridging uneven cash flow

Jon gets paid in crypto, but his expenses don't arrive on a crypto-friendly schedule. Rent, tax obligations, software bills, and contractor payments show up when they show up.

Borrowing can bridge that mismatch. Instead of selling assets every time a bill lands, he can use a collateralized loan to cover short-term needs and repay when client payments settle. In traditional personal finance, people often use borrowing to reorganize expensive obligations too. If you're comparing off-chain options for that kind of problem, DebtBusters' guide to credit card debt solutions gives a practical look at when a personal loan may be more sensible than revolving card debt.

The small DAO preserving treasury optionality

A DAO often holds treasury assets it doesn't want to dump into a weak market. But contributors still need to be paid, and operations still need funding.

Borrowing lets the DAO access working capital without forcing a treasury sale at a bad time. This is one of the strongest strategic uses of on-chain credit because the alternative is often reactive selling.

Modern lending systems are getting better at this kind of risk-based design. Data-driven lending engines increasingly assess borrower quality through richer signals, and DeFi protocols are starting to use on-chain history to inform risk parameters, as discussed in this overview of modern lending technology and data-based underwriting. That trend matters because better risk assessment can lead to more capital-efficient borrowing over time.

For teams comparing options, this roundup of the best crypto lending platforms can help narrow the field.

The best borrowing strategy is usually boring. It solves a cash problem, preserves flexibility, and avoids forcing a sale. It doesn't need heroic assumptions.

The Final Decision When to Borrow vs When to Earn

Most stablecoin holders don't need a lecture on financial theory. They need a decision rule. Borrowing and earning are both valid tools, but they're built for different jobs.

Borrowing is active. Earning can be much more passive. Borrowing gives you liquidity without selling, and sometimes magnified investment capacity. Earning aims to grow idle stablecoins without creating debt that needs oversight.

Choose borrowing if your goal is access and flexibility

Borrowing makes sense when all three of these are true:

You need liquidity now but don't want to sell an asset.

You understand the collateral risk and can manage it.

You have a defined use for the borrowed funds.

This is the right mindset for someone managing treasury timing, bridging cash flow, or preserving a core position through a short-term need.

Choose earning if your goal is compounding with less friction

Earning is usually the cleaner choice when:

Question | Borrowing | Earning |

|---|---|---|

Do you need cash today? | Often yes | Usually no |

Will you monitor a position closely? | You should | Less constant oversight |

Is your main objective leverage or liquidity? | Yes | No |

Is your main objective steady growth on idle stablecoins? | Not ideal | Better fit |

The hidden cost in borrowing isn't only interest. It's attention. A borrowing position asks for monitoring, judgment, and readiness when markets move. A yield strategy asks you to evaluate different risks, but it usually doesn't force the same kind of real-time collateral management.

Use scenario thinking, not impulse

A good finance habit is to model multiple futures before committing capital. That isn't only for CFOs. It's useful for anyone deciding whether to borrow against assets or put stablecoins to work. This short note on strategic financial foresight for businesses is a smart reminder to build a base case, an upside case, and a stress case before making a big money decision.

Ask yourself:

What happens if my collateral falls sharply?

What happens if I need this cash longer than expected?

What happens if I don't borrow and earn instead?

If the stress case breaks your plan, the strategy isn't ready.

Borrowing is powerful when you need control over timing. Earning is powerful when you want your stablecoins working without turning your wallet into a liability stack. The right choice depends less on what's “better” in the abstract and more on what job your capital needs to do this month.

If your goal is to put idle stablecoins to work without actively managing borrowing positions, Yield Seeker offers an AI-powered way to earn automated, risk-aware yield on stablecoins. You can start with as little as $10 USDC on Base, keep funds accessible, and let the platform handle the constant protocol monitoring that most busy holders don't have time to do themselves.