Your stablecoins can sit in a wallet for months and do nothing. That feels safe, but idle cash has a cost. In crypto, the bigger cost is often missed opportunity. The tools to earn yield exist, but individuals often run into the same wall fast: too many protocols, too many moving parts, and too much risk to manage casually.

That’s where lending protocols matter. They’re the quiet infrastructure behind a large share of onchain yield. If you hold USDC and want it working without turning portfolio management into a second job, this is usually where the conversation starts.

Your Guide to DeFi Lending Protocols

Stablecoin holders usually want three things at once. They want yield, they want access to their funds, and they don’t want to babysit positions all day. Traditional savings products rarely satisfy crypto-native users, but manually farming DeFi yield often swings too far in the other direction.

Lending protocols sit in the middle. They let lenders deposit assets into shared pools, and they let borrowers post collateral to borrow against those pools. That basic exchange is simple. The hard part is choosing where to lend, when rates are attractive, and how to avoid the hidden failure modes.

A lot of newcomers first need a clean conceptual map before they touch anything onchain. If you want that foundation, The Coin Course has useful DeFi lending insights for newcomers that explain the basic flow without drowning you in jargon.

What matters in practice is this:

Idle stablecoins earn nothing: If USDC is just sitting in a wallet, you keep custody, but you don't generate return.

Lending protocols create passive income paths: You supply assets, the protocol routes borrowing demand through the pool, and interest flows back to suppliers.

A key challenge is operations: Rates move, risk parameters differ by market, and what looked safe last week may be inefficient today.

Practical rule: In DeFi, the easy part is depositing. The hard part is knowing whether the yield is still worth the risk tomorrow morning.

That’s why busy professionals often struggle here. The mechanics are transparent, but transparency doesn't remove complexity. It just puts the complexity in plain sight.

What Are Lending Protocols

Lending protocols match two groups onchain: people who want yield on idle assets, and people who want liquidity without selling what they already hold. The rules live in smart contracts, so deposits, borrowing limits, interest accrual, and liquidations happen according to code instead of a credit team.

That structure matters for stablecoin holders.

If a treasury manager, founder, or active DeFi user is sitting on USDC, a lending protocol is often the first place to look for base yield. You supply stablecoins to a pool. Borrowers post collateral and pay to access that liquidity. Suppliers earn a share of that demand. The appeal is obvious. The work starts after the deposit, because each market has different usage patterns, collateral quality, and failure modes.

The two sides of the market

Lenders supply assets such as stablecoins and earn yield from borrowing activity in that pool. Their job is simple in theory and harder in practice: find demand strong enough to pay, without stepping into a market that can freeze withdrawals or suffer bad debt under stress.

Borrowers come for different reasons. Some want working capital without selling ETH or BTC. Some want stablecoins for trading or hedging. Some are running spread trades across multiple protocols. They post collateral first, then borrow within the limits the protocol allows.

The protocol sits between them and enforces the rules. Its main purpose is solvency. If that discipline breaks, the yield disappears fast.

Lenders focus on rate quality and withdrawal safety: A high APY means less if liquidity dries up when they want out.

Borrowers focus on usable credit: They want as much borrowing power as possible without getting pushed into liquidation by a routine price move.

Protocols focus on keeping the pool whole: Risk parameters, collateral factors, and liquidation rules exist to protect lenders first.

Why these protocols feel different from a bank

Banks bundle the complexity behind internal balance sheets, policy teams, and opaque underwriting. Lending protocols expose the machinery. Users can inspect supported assets, collateral settings, pool utilization, and rate models in public.

Open visibility helps, but it does not reduce the operational burden. It shifts that burden to the user.

For anyone trying to earn stablecoin yield consistently, that is the primary friction. The opportunity is easy to understand. The day-to-day management is not. Rates move. Liquidity fragments across protocols. Risk can rise even while the interface still looks calm. That is why AI-driven systems such as Yield Seeker make sense in this category. They do not change how lending protocols work. They help monitor markets, compare opportunities, and react faster than a manual workflow.

Why stablecoin users pay attention

Lending protocols are one of the cleanest ways to put stablecoins to work onchain. You are supplying liquidity to a market with ongoing borrowing demand, not relying on token appreciation to generate return.

That sounds straightforward, and sometimes it is. But stablecoin yield is only attractive if it stays net positive after risk, monitoring time, and movement costs. In practice, the hard part is not finding a pool. The hard part is choosing one you can trust, then knowing when conditions have changed enough to move.

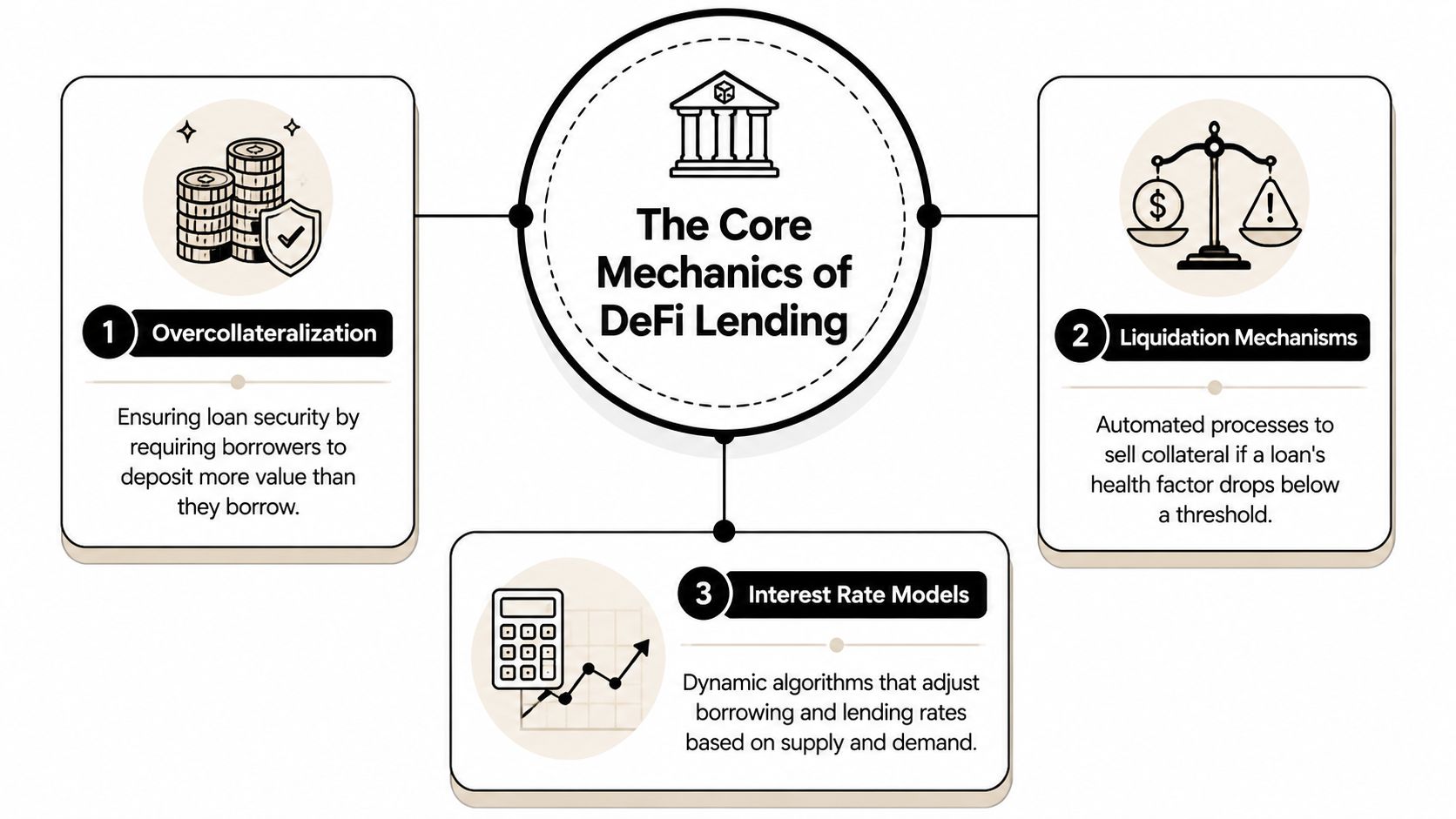

The Core Mechanics of DeFi Lending

You deposit USDC expecting a steady yield. A week later, the rate drops, one pool is suddenly hard to exit, and another is paying more for reasons that are not obvious from the dashboard. That confusion usually comes from not seeing the three systems underneath the APY: collateral rules, liquidation logic, and utilization-based rates.

Overcollateralization sets the boundary

Pool-based lending protocols such as Aave and Compound do not underwrite borrowers the way a bank would. They rely on posted collateral and preset risk parameters. The key number is the loan-to-value ratio, or LTV. If a market allows 75% LTV, a user who deposits $1,000 of ETH can borrow up to $750 against it, as explained in Chainlink’s overview of decentralized lending protocol parameters.

For lenders, this buffer is the first line of defense. For borrowers, it defines how much room they have before market volatility turns into a problem.

Liquidation enforces the rules

LTV tells a borrower how far they can go. The liquidation threshold tells the protocol when to step in.

Using the same example, a borrower posts $1,000 of ETH and borrows $750 of USDC. If ETH falls enough and the health of that position deteriorates past the protocol’s threshold, liquidators can repay part of the debt and buy the collateral at a discount. The process is automatic because manual enforcement would be too slow in a volatile market.

That mechanism protects suppliers from absorbing unsecured losses.

A practical way to read it is simple:

LTV defines initial borrowing power

Collateral price moves change position health

Liquidation closes risk before the pool becomes insolvent

If you are lending stablecoins, this matters even if you never borrow. Your yield depends on the protocol being able to remove bad debt quickly.

Dynamic rates react to pool usage

The third part is the interest rate model. Rates move with utilization, which is the share of supplied assets that borrowers have already taken out. When utilization is low, suppliers usually earn less because borrowing demand is weak. When utilization climbs, rates rise to attract new deposits and push some borrowers to repay.

Many major protocols use a kink-based model. Rates increase gradually until utilization reaches a target zone, then rise much faster once the pool gets crowded, as described in Metalamp’s developer guide on how DeFi lending protocols work.

In practice, stablecoin yield gets harder. A high rate can mean strong demand. It can also mean the pool is stressed, withdrawal liquidity is thinner, and conditions can change fast.

Why these mechanics matter for stablecoin yield

For a stablecoin lender, the job is not just to find the highest APR. The job is to judge whether that rate is worth the protocol risk, liquidity conditions, and the time required to monitor it.

A calm-looking pool can still be a poor choice if utilization is pinned high, collateral in the market is volatile, or better risk-adjusted opportunities exist elsewhere. That is why experienced users track the mechanics under the headline number, and why automated systems such as Yield Seeker are useful. They monitor rate shifts, utilization pressure, and cross-protocol opportunities faster than a manual workflow.

If you want a broader view of where these mechanics show up in practice, this comparison of crypto lending platforms for earning yield is a useful reference.

A Look at Popular Lending Protocols

A lender moving stablecoins between protocols usually starts with a simple question: where is the yield better today? In practice, the better question is narrower. Which protocol gives acceptable yield for the kind of risk, liquidity profile, and monitoring burden you can handle?

For most users, that comparison starts with Aave and Compound because both sit at the core of DeFi credit markets and both are familiar enough to price quickly.

Protocol Comparison Aave vs. Compound

Feature | Aave | Compound |

|---|---|---|

Core model | Pool-based lending markets | Pool-based lending markets |

User position | Known for its aToken model | Known for its cToken model |

Governance style | Broad protocol governance with active parameter design | Governance-led approach centered on market parameters |

Typical user fit | Users who want broad market options and mature DeFi infrastructure | Users who prefer a simpler lending experience with established markets |

Market identity | Often associated with feature expansion and deeper DeFi integrations | Often associated with straightforward lending and borrowing primitives |

The point is fit, not brand preference. Aave often appeals to users who want more assets, more integrations, and more ways to put idle capital to work across DeFi. Compound usually appeals to users who want a cleaner lending setup with fewer moving parts.

For a stablecoin lender, that difference matters because operational complexity is part of the cost. A protocol with more features can create more opportunities, but it can also require closer attention to market configuration, liquidity conditions, and governance changes. If you want a wider platform comparison before allocating capital, this guide to best crypto lending platforms is a useful reference.

What separates the major overcollateralized protocols

Aave and Compound both use overcollateralization. Borrowers post more value than they borrow, and the system relies on liquidation rules instead of reputation checks. That makes these markets easier to evaluate for stablecoin yield because the core risk inputs are visible onchain.

In practice, three factors matter more than small differences in interface or branding:

Market depth: Large pools usually handle entries and exits with less friction.

Asset mix: Demand depends on which collateral and borrow assets are listed.

Risk management: Conservative parameters and disciplined governance matter more than headline incentives.

The boring option is often the better one. For steady stablecoin income, mature markets with predictable behavior usually beat newer markets offering a temporary rate spike.

The rise of undercollateralized lending

A different branch of DeFi lending tries to increase capital efficiency by reducing or removing the need for full collateral. Protocols such as Maple, TrueFi, and Goldfinch use credit assessment, delegated underwriting, or borrower screening instead of relying only on liquidation logic. Cherry’s analysis of uncollateralized lending in DeFi explains how that model shifts risk toward third-party judgment and recovery processes.

That changes the job for the lender. In an overcollateralized market, the main questions are usually mechanical: collateral quality, utilization, liquidation design, and pool liquidity. In an undercollateralized market, lenders also have to assess who is making credit decisions, how losses are absorbed, and what happens if repayment depends on offchain enforcement.

I would automate overcollateralized stablecoin allocation long before I would automate credit exposure with the same confidence. Software can monitor rates, utilization, and collateral conditions well. It is much weaker at judging borrower quality, legal recovery odds, or underwriting discipline from one credit pool to the next.

That trade-off matters if the goal is stablecoin yield you can manage at scale. Overcollateralized protocols are usually easier to compare, rebalance, and automate. Undercollateralized protocols can offer attractive returns, but they add judgment risk, which is exactly where AI systems like Yield Seeker need tighter rules, narrower mandates, and more human oversight.

Navigating the Risks of Lending Protocols

Yield from lending protocols isn't free money. It’s payment for taking risk that someone else doesn’t want to hold. As the category has grown, the need to understand that risk has become more urgent. DeFi lending reached a new all-time high of $73.59 billion in total value locked at the end of Q3 2025, according to CEPR’s analysis of DeFi lending motivations, risks, and investor behaviors.

When that much capital sits inside smart contracts, mistakes stop being academic.

Smart contract risk

Every lending protocol is software. If the code has a flaw, a user can lose money even if their market view was correct.

This is the risk many newcomers underestimate because a clean interface feels familiar. But the frontend is only the dashboard. The actual exposure sits in contract logic, upgrade paths, admin controls, and integrations.

A practical response is to favor protocols with a long operating history, conservative design, and clear security processes. That doesn't eliminate risk. It narrows the set of surprises.

Oracle and parameter risk

Lending protocols need price data to decide whether collateral is healthy. If the oracle is wrong, slow, or manipulated, liquidations can happen at the wrong time or fail when they should trigger.

Parameter risk is quieter but just as important. A protocol can support a volatile asset with rules that are too generous. That can work for a while, then break during stress.

Bad data leads to bad enforcement: If the protocol thinks collateral is worth more or less than reality, user positions can be handled incorrectly.

Loose parameters attract volume: They also increase the chance that lenders absorb pain during fast markets.

Users rarely monitor both continuously: That’s why manual strategies often drift into riskier territory than intended.

Liquidity risk

This is the risk stablecoin users feel first. You deposit into a pool because the APY looks attractive. Then utilization rises, conditions tighten, and withdrawing may become less convenient than you expected.

A high yield often signals one of two things: strong demand or increased stress. Sometimes both.

For a deeper operational checklist on this side of the market, it helps to review a dedicated guide to DeFi risk management.

A lending position can look safe at entry and still become annoying to manage. The pain usually comes from monitoring burden, not from one dramatic event.

That’s the manual workload often not priced in. To do this well, you need to track protocol quality, market utilization, collateral behavior, and changing incentives. That's manageable for a full-time DeFi operator. It’s much less manageable for someone with a job, a treasury, or ten other priorities.

Automating Your Yield with AI Agents

The operational problem in lending protocols is simple to state and tedious to solve. The best opportunities move. Risk conditions move. Utilization moves. Most users don't want to open five dashboards every day to decide whether their USDC should stay where it is.

That’s where an automation layer starts to make sense.

What an AI agent actually does

An AI agent for yield doesn't magically remove protocol risk. What it does is handle the work that most humans perform inconsistently. It watches conditions, compares routes, and reallocates capital based on the rules you set.

That’s a useful fit for stablecoin lending because the edge often comes from responsiveness, not prediction. If rates rise in one pool and liquidity deteriorates in another, the user who reacts quickly often earns better risk-adjusted returns.

A good mental model is an autopilot with guardrails. You still choose the route and risk posture. The system handles the repetitive monitoring and execution.

Why context matters in automation

The quality of an agent depends on what context it uses. It has to understand protocol conditions, available liquidity, and your constraints, then act without creating unnecessary churn. If you want a good framework for that design problem, Prompt Builder’s 2025 guide is worth reading because it explains why agent behavior depends so heavily on structured context, not just generic prompts.

That idea maps directly to DeFi. A yield agent that only chases headline APY is incomplete. A useful one needs to weigh access, concentration, changing utilization, and the user's own boundaries.

Where this becomes practical for stablecoin users

For a hands-off user, the cleanest version is straightforward. Deposit USDC. Set risk preferences. Let the system monitor lending markets and allocate accordingly.

One example is how to use AI agents in a setup where the user deposits USDC on Base and an agent monitors and allocates capital across lending protocols in real time. The value isn't that automation makes DeFi effortless in some magical sense. The value is that it compresses a messy operating job into a repeatable workflow.

Here’s a simple walkthrough of the concept in action:

What works and what doesn't

Automation works well when the task is repetitive, rule-based, and time-sensitive. Lending protocol allocation fits that profile.

It works poorly when users expect it to erase all risk or make judgment calls without constraints.

What works: Monitoring utilization, scanning supported pools, reallocating stablecoins, and reducing dashboard fatigue.

What doesn't: Blindly chasing the highest number on screen without considering protocol quality and withdrawal conditions.

What matters most: Clear rules, narrow scope, and transparent execution.

For busy professionals, this is the key benefit. Not “AI” as a slogan. Reliable systems that keep stablecoins productive without requiring constant manual intervention.

Common Questions About Earning Yield

How are earnings from lending protocols usually taxed

Tax treatment depends on where you file and what you received. Interest, token incentives, and swaps can each be treated differently. The practical answer is simple. Track every deposit, withdrawal, reward, and conversion from the start, because rebuilding that history later is slow and error-prone.

How does an automated platform keep funds secure

Security starts with structure, not marketing claims. Check who controls the wallet, whether the strategy uses only approved protocols, and whether you can see what the system is doing with your funds. Good automation reduces manual mistakes, but it does not remove smart contract risk, bridge risk, or liquidity constraints. You still need clear rules for where capital can go and how fast it can be pulled back.

What's a sensible amount to start with

Start with an amount that lets you test the full cycle without second-guessing every market move. Deposit, watch how interest accrues, review any reallocations, and do a withdrawal. That process teaches more than staring at APY tables.

Small first deposits also make risk feel concrete. You learn how the product behaves when rates change, when a pool fills up, or when you want funds back quickly.

Why does yield change so often

Because the demand for borrowed stablecoins changes constantly.

Lending rates are not fixed coupons. They react to borrower activity, available liquidity, and the rules each protocol uses to price capital. A pool that looks attractive in the morning can look average by the afternoon if borrowers leave, lenders pile in, or incentives expire.

That is the hard part for anyone trying to earn stablecoin yield consistently. The job is not just finding a decent rate once. The job is monitoring whether that rate still makes sense after fees, liquidity conditions, and protocol risk. That is also why AI-driven automation is useful here. Systems like Yield Seeker can watch those moving parts continuously and apply pre-set rules faster than a person checking dashboards between meetings.

If you want a simpler way to put stablecoins to work, Yield Seeker offers an AI-powered workflow for depositing USDC on Base and letting an agent monitor and allocate across DeFi lending opportunities in real time, with funds remaining accessible as your needs change.