Back to Blog

Earn Interest on Stablecoins: Boost Your Passive Income

Learn how to earn interest on stablecoins safely. Discover top platforms, strategies, and tips to maximize your passive income today!

Jun 26, 2025

published

So, what's the deal with earning interest on stablecoins? Put simply, it’s a way to put your crypto to work. You lend out stable assets like USDC or USDT through various platforms and, in return, you collect rewards. This approach can offer much more attractive yields than you'd ever see from a traditional bank, turning your digital dollars into a real source of passive income. It's one of the core ideas in Decentralized Finance (DeFi) and, thankfully, it's become incredibly easy to get started.

Why Stablecoin Interest Leaves Traditional Savings in the Dust

If you’ve ever glanced at your bank statement and felt a bit underwhelmed by the pennies trickling into your savings account, you're definitely not alone. The real magic of earning with stablecoins is just how much better the returns can be. We're talking about a completely different league. A "high-yield" savings account at a bank might give you 4-5% APY if you're lucky, but the digital asset world plays by different rules.

And this isn't some complex trading strategy where you have to perfectly time the market. It's much more straightforward. You're simply providing your stablecoins to a platform, which then lends them out to traders and others who need liquidity. For providing that service, you get paid interest.

The fundamental difference comes down to efficiency and raw demand. DeFi and centralized crypto platforms don't have the massive overhead of brick-and-mortar banks. This means they can pass a much larger slice of the lending profits straight back to you.

Just Look at the Numbers

The numbers really do speak for themselves. The gap between what a bank offers and what you can earn on stablecoins isn't just a few percentage points—it’s often a massive leap. This potential is what pulls so many people into exploring stablecoin yields as a core part of their passive income strategy.

Before we go further, let's put this into perspective with a quick comparison.

Stablecoin Yield Potential vs. Traditional Savings

Asset Type | Platform / Account Type | Potential Annual Percentage Yield (APY) | Key Conditions |

|---|---|---|---|

Stablecoins | DeFi Lending (e.g., Aave) | 5-15% | Variable rates based on demand; requires self-custody. |

Stablecoins | CeFi Platform (e.g., Nexo) | Up to 16% | Often requires locking tokens or holding platform token. |

USD | High-Yield Savings Account | 4-5% | Rates can change; often has deposit limits. |

USD | Standard Bank Savings | ~0.45% | FDIC insured; extremely low returns. |

As you can see, even the more conservative stablecoin yields significantly outperform what traditional banks are offering. For example, some platforms have offered rates as high as 16.00% APR on stablecoins like USDT if you're willing to lock up your assets for a fixed term. Even the base rates often sit comfortably around 9.00% APR, which is still miles ahead of old-school finance. You can easily explore a comparison of these rates to see how different stablecoins are performing across various platforms.

The incentive is clear. Why let your money sit idle when it could be actively generating returns for you in the crypto ecosystem?

How Does It Actually Work?

Think of yourself as a mini-bank, but without the skyscraper and stuffy suits. When you deposit money in a savings account, the bank lends it out and gives you a tiny fraction of the profits. By depositing stablecoins on a lending platform, you're cutting out that expensive middleman.

Here’s a simple rundown of the process:

You deposit your stablecoins (like USDC or USDT) into a lending protocol or a centralized exchange.

Borrowers take out loans using your assets and pay interest for the privilege.

You earn interest as the platform collects it from borrowers and distributes a large portion back to you and the other lenders.

This entire system is fueled by the massive demand for stablecoin liquidity in the crypto market. Traders, DeFi protocols, and even institutions need stable assets for everything from making trades to hedging against volatility. Your deposits help keep this engine running, and you're rewarded for it. It's this dynamic that makes earning interest on stablecoins such a powerful and accessible strategy for building wealth.

Choosing the Right Stablecoin and Platform

Before you can start earning, you've got two big decisions to make: which stablecoin to hold and which platform to trust with it. These aren't minor details; they directly shape your potential returns, your risk, and just how complicated this whole thing gets. Getting this right from the start makes everything else that follows much smoother.

You might think all stablecoins are the same because they all aim for that $1 peg, but they're built very differently. Understanding what's under the hood is your first line of defense.

Comparing the Top Stablecoins

Let's break down the big players you'll run into almost everywhere.

USDC (USD Coin) is often seen as the "safe" choice. It's built with regulation and transparency in mind, fully backed by cash and short-term U.S. government bonds. They even get monthly check-ups from major accounting firms. If you prioritize safety and sleeping well at night, this is usually your go-to.

USDT (Tether) is the behemoth. It has the largest market cap and you can use it on pretty much any platform you can think of. The trade-off? Its history with reserve transparency has been a bit murky, which makes some experienced users cautious despite its massive liquidity.

DAI is the odd one out, but in a good way for DeFi purists. It's a decentralized stablecoin, meaning instead of being backed by dollars in a bank account, it's over-collateralized by a basket of other crypto assets locked in smart contracts. This is true to the core spirit of DeFi, but it also brings its own set of risks, like the stability of its collateral.

So, it's a classic trade-off. USDC brings peace of mind, USDT offers unmatched access, and DAI delivers on the decentralized dream. What you pick really comes down to your personal risk tolerance.

CeFi vs. DeFi: Where to Earn Your Yield

Once you've got your stablecoin, where do you put it? The crypto world splits this into two main camps: Centralized Finance (CeFi) and Decentralized Finance (DeFi). Each one offers a very different way to earn interest.

Centralized Finance (CeFi) platforms like Nexo operate a lot like a crypto-savvy bank. You deposit your funds with a company, and they do the heavy lifting.

CeFi's Main Appeal: Think of it as the "easy button" for crypto yield. The apps are typically slick, there's customer support if you get stuck, and some even provide insurance. But this convenience comes with a catch: you're handing over your keys. You have to trust the company to keep your funds secure.

Decentralized Finance (DeFi) platforms, such as Aave and Compound, are a different beast entirely. They run on public blockchains, powered by smart contracts. You never give a company control of your funds; you interact directly with the code.

This route gives you full control and total transparency, but it also means you're on your own. You are your own bank, which also means you're responsible for your own security. If you want to dive deeper into the strategies popping up in this space, the Yield Seeker blog is a great place to explore.

Interest rates can swing wildly between all these platforms, all driven by simple supply and demand. For instance, you might see USDT earning around 3.59% APY on Compound, but on Aave, the rates could be much more attractive: USDT at 5.68% APY, USDC at 7.33% APY, and DAI hitting a massive 11.64% APY. To stay on top of this, it's worth taking the time to compare stablecoin interest rates across different platforms to see who's offering what and why.

Take a look at the screenshot below—it shows just how much the yields can differ for the same stablecoins across DeFi's top protocols.

This data really shines a light on the premium being paid for DAI inside the Aave protocol. It’s a strong signal of the market's confidence in decentralized stablecoins for borrowing and lending. Ultimately, your choice will be a balance between chasing the highest yield and how comfortable you are with a platform's security and your own technical skills.

Alright, let's get your digital dollars to work. Enough with the theory—it's time to see this in action. We're going to walk through the whole process, from getting your hands on some stablecoins to making your first deposit and earning interest.

I'll use Aave as our main example. It’s one of the oldest and most trusted DeFi lending protocols out there, so it's a solid place to start.

First, Get Your Stablecoins

Before you can earn anything, you need some capital. The most direct path for this is a big, reputable centralized exchange (CEX) like Coinbase or Kraken. Think of these as the on-ramps from your bank account to the crypto world.

The process is pretty much the same everywhere:

Sign up and get verified. You'll need to provide some ID to meet regulatory requirements. It's standard stuff.

Deposit your cash. Link your bank account or use a debit card to move funds like USD or EUR onto the platform.

Buy your stablecoins. Head over to their "buy crypto" or trading section, find a stablecoin like USDC, and make the purchase. Just like that, the stablecoins will be sitting in your exchange account.

Now, a pro tip: don't leave your funds sitting on an exchange long-term. You don't actually control the private keys, which means they're not truly your funds. The next step is to move them somewhere you have full control.

Set Up a Wallet You Actually Control

To play in the world of DeFi, you need what’s called a non-custodial or self-custody wallet. This just means you—and only you—hold the keys. The go-to choice for most people is MetaMask. It’s a simple browser extension that makes it easy to connect to apps like Aave.

Setting it up is straightforward, but you need to pay close attention to one critical step. You'll be given a secret recovery phrase (sometimes called a seed phrase).

Listen up, this is important: Write this phrase down on a piece of paper. Store it somewhere safe and offline. Never, ever save it as a screenshot, in a text file, or in the cloud. If you lose this phrase, your money is gone. If someone else finds it, your money is gone. It's the master key to everything.

Once MetaMask is set up, withdraw your stablecoins from the exchange. You'll copy your MetaMask wallet address and paste it into the withdrawal field on the exchange. Always, and I mean always, double-check the first and last few characters of the address before hitting send. A typo here means your funds are sent into the void, forever. You'll also need to select the right blockchain network for the transfer (like Ethereum, Polygon, or Base).

Make Your First DeFi Deposit on Aave

With your stablecoins now safe in your MetaMask wallet, you're ready for the main event: depositing into Aave to start earning.

Head over to the Aave app website. It will ask you to connect your wallet. Choose MetaMask, and a little pop-up will ask you to approve the connection. Once you're in, you'll see a dashboard with all the different assets you can supply (lend) or borrow.

Find the stablecoin you're holding (let's say USDC) and look for the "Supply APY." That's your interest rate.

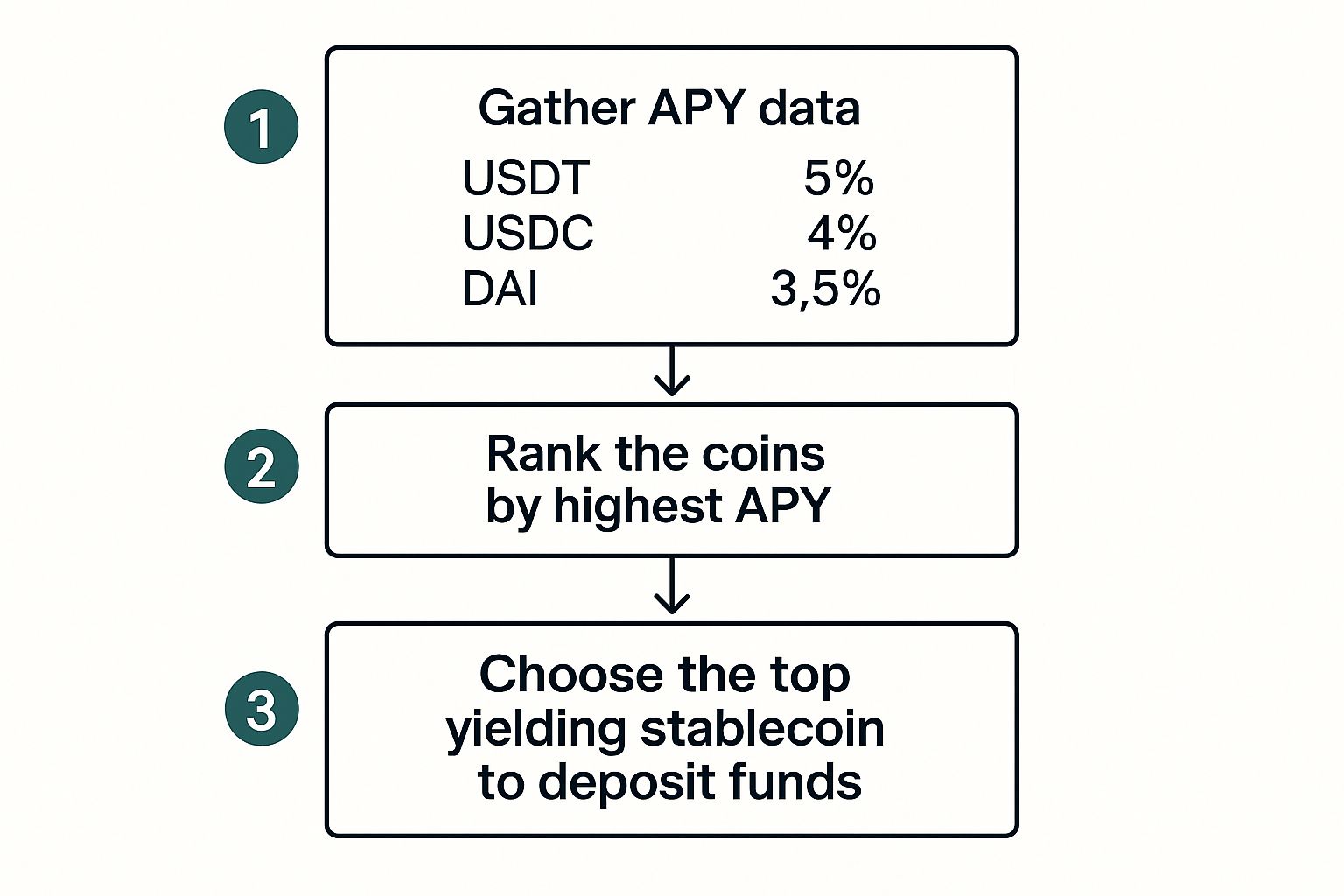

The infographic below shows a pretty simple way to think about which asset to choose based on the current rates.

As you can see, sometimes it’s as simple as picking the one with the highest number next to it.

To get your funds in, you'll need to make two separate transactions:

Approve: The first transaction is just you giving the Aave smart contract permission to access the USDC in your wallet. It's a standard DeFi security step, and you only have to do it once for each coin you deposit.

Supply: This is the actual deposit. You'll type in how much you want to supply, confirm it, and you're good to go.

Both of these steps will cost a small "gas fee," which is what you pay the network to process your transaction. These fees change depending on how busy the network is.

After your supply transaction is confirmed on the blockchain, that’s it! You'll start earning interest immediately. You can even watch your balance tick up in real-time right on the Aave dashboard.

How to Manage Your Stablecoin Risks

The high yields you can get when you earn interest on stablecoins look incredibly tempting, but let's be real—they don't come for free. The single most important part of building a sustainable passive income strategy in crypto is understanding and actively managing the risks involved. Ignoring them is like driving without a seatbelt. It might be fine for a while, but it’s a disaster waiting to happen.

The good news is that these risks are pretty well-understood, and you can take clear, practical steps to protect your capital. It all starts with knowing what you’re up against.

The Big Three Stablecoin Risks

When you put your money to work in DeFi or CeFi, there are three main places things can go sideways. Each one needs a different way of thinking and a different strategy to handle it.

Smart Contract Risk: This is the big one in the DeFi world. The protocols you use, like Aave or Compound, are ultimately just code. If a hacker finds a bug or an exploit in that code, they can potentially drain the funds. It’s happened before, and it will definitely happen again.

Platform (Counterparty) Risk: This is your primary concern with CeFi platforms. You are trusting a company to hold your assets. If that company goes belly up, mismanages its funds, or gets hacked, your stablecoins could be gone for good. You’re essentially swapping code risk for company risk.

De-pegging Risk: This is when a stablecoin fails to hold its $1 peg. It can happen for all sorts of reasons—a loss of confidence in its reserves, a flaw in its stabilization algorithm (a classic problem for algorithmic stablecoins), or just a massive market panic.

These aren't just hypotheticals. We’ve all seen major platforms collapse and popular stablecoins lose their peg, wiping out billions in user funds. This is exactly why active risk management is non-negotiable.

The core idea behind crypto risk management isn't finding a "no-risk" unicorn—that doesn't exist. It's about layering your defenses. By diversifying and doing your homework, you can dramatically reduce your exposure to any single point of failure.

Smart Strategies for Staying Safe

Okay, on to the practical stuff: how do you actually defend against these threats? It really boils down to two things: doing your due diligence and not putting all your eggs in one basket.

Your most powerful tool, by far, is diversification. Never, ever go all-in on a single platform or a single stablecoin. If you have $10,000 to put to work, think about splitting it up.

You could put $4,000 of USDC on Aave.

Another $4,000 of USDT on a different, well-regarded protocol.

And maybe keep the remaining $2,000 in a centralized, insured account as a safer base.

This simple split immediately insulates you from a single platform-specific or coin-specific disaster. Your entire stack is no longer vulnerable to one smart contract bug or one company’s poor decisions. For a deeper dive, our guide on stablecoin staking strategies shows how to effectively balance different assets and platforms.

Vet Projects Like an Investor

Before you deposit a single dollar, you need to do your homework. Look for the signs of a healthy, security-focused project.

Check for Audits: Reputable platforms will pay to have their smart contracts audited by well-known security firms like CertiK, Trail of Bits, or OpenZeppelin. An audit isn't a 100% guarantee of safety, but a lack of one is a massive red flag.

Understand the Collateral: For stablecoins, you have to know what's backing them. Is it cash and U.S. T-bills, like with USDC? Or is it a basket of other, more volatile crypto assets, like DAI? The type of collateral directly impacts its ability to stay stable during market chaos.

Look at TVL and History: A platform's "Total Value Locked" (TVL) and how long it's been around can be great indicators of trust. A protocol that has securely managed billions of dollars for several years is generally a much safer bet than a brand-new project promising absurdly high yields.

By combining smart diversification with thorough research, you build a robust defense. This lets you confidently earn interest on your stablecoins while seriously minimizing the chances of a catastrophic loss.

Tracking and Optimizing Your Crypto Earnings

Getting your stablecoins deployed and earning interest is a great start, but it's really just the beginning. If you want to get the most out of your capital, you can't just "set it and forget it." The real pros actively manage their positions, always on the lookout for ways to squeeze out more yield.

Think of yourself as the manager of your own little fund. You need to keep an eye on performance, understand how your money is growing, and know exactly when it's time to make a move.

Understanding How Your Interest Compounds

Compounding is where the magic really happens, letting your earnings generate their own earnings. But how this works can vary wildly from one platform to another.

Automated Compounding: This is the easy mode. Many centralized platforms (CeFi) and some of the more sophisticated DeFi vaults handle this for you. Your interest gets rolled right back into your principal deposit automatically. No fuss, no fees.

Manual Compounding: In a lot of core DeFi protocols, like Aave for instance, your earned interest just sits there waiting for you. To get it compounding, you have to manually "claim" it and then redeposit it into the pool. This, of course, costs gas.

When you have to compound manually, you've got a simple decision to make: is it worth the fee? If you've only earned a few dollars in interest, a $5 gas fee will wipe out your gains. A good rule of thumb is to wait until the gas fee is just a tiny fraction of the interest you've accrued.

Using Portfolio Trackers to See Everything

Once you start spreading your capital across a few different protocols and maybe even a couple of blockchains, things get messy fast. Logging into five different websites to check your balances is a surefire way to miss something important. This is where portfolio trackers become your best friend.

Portfolio trackers are your command center for DeFi. They pull data from various blockchains and protocols to give you a single, unified view of all your assets, debts, and yield-farming positions. This clarity is crucial for making smart, timely decisions.

Tools like DeBank and Zapper are essentials in the space. You just paste in your wallet address, and they give you a complete picture of your net worth and where every single stablecoin is parked. You can instantly spot which positions are crushing it and which ones are lagging.

For an even smoother experience, our own visual guide at Yield Seeker shows how an integrated dashboard pulls all this together, making management a breeze.

The Art of Rotating Your Capital

DeFi moves at lightning speed. The best yields today might be mediocre tomorrow. The most successful yield farmers are constantly "rotating" their capital, moving funds from one protocol to another to chase the highest rates.

For example, you might see a pool on the Base network offering a juicy 9% APY on USDC. If your current spot on another chain is only pulling in 6%, making a switch seems like a no-brainer.

But hold on. Every rotation comes with costs. You'll likely pay fees to withdraw from the old protocol, bridge your funds to the new chain, and deposit into the new pool. You have to run the numbers. Will the extra 3% you earn cover those transaction costs and still leave you with a profit in a reasonable amount of time?

This constant movement is becoming more common. We're seeing a huge rise in the velocity of stablecoins like PYUSD and USDC as they're used for more than just holding—they're active assets for liquidity and payments. You can read more about these stablecoin trends to see just how dynamic the market is.

By getting a handle on these tracking and optimization techniques, you can turn a simple plan to earn interest on stablecoins into a sophisticated and much more profitable strategy.

Your Burning Stablecoin Questions, Answered

As you get ready to dive into earning with stablecoins, a few questions always pop up. It's totally normal to want to get the details straight, especially when your money is on the line. I've put together the most common queries I hear about taxes, security, and just how those impressive yields are even possible.

Let's clear up any lingering doubts so you can move forward feeling confident and knowing exactly what you're getting into.

What's the Deal with Taxes on Stablecoin Interest?

This is usually the first question on everyone's mind, and for good reason. In most places, like the US, any interest you earn from stablecoins is considered a taxable event. The income you pocket is typically treated as ordinary income—no different from the interest you'd get from a regular bank savings account.

You're required to report this on your tax returns. The value of that interest is based on its fair market value on the day it hits your wallet. This means keeping meticulous records isn't just a good habit; it's absolutely essential to stay on the right side of the law.

To stay on top of it, here's what I recommend:

Track Everything: Keep a detailed log of every single interest payment. Note the date, the amount of stablecoin you received, and its dollar value at that exact moment.

Use Crypto Tax Software: Tools built specifically for crypto taxes can plug into your wallets and exchanges. They automatically track these taxable events and make reporting a whole lot less painful.

Talk to a Pro: Honestly, the smartest move is to speak with a qualified tax advisor who actually has experience with cryptocurrency. Tax laws are a minefield and change depending on where you live, so getting professional advice is worth its weight in gold.

How Safe Is It, Really, to Lend Out My Stablecoins?

Safety in crypto isn't a simple yes or no—it's a spectrum, and it all comes down to the choices you make. The biggest factors are the platform you use and how comfortable you are with different types of risk.

Centralized Finance (CeFi) platforms often feel safer, especially for newcomers. They usually have slick apps, customer support teams, and sometimes even offer insurance on your deposits. But that convenience comes with a trade-off: custodial risk. You're trusting a company to hold onto your funds for you.

On the other hand, Decentralized Finance (DeFi) platforms run on open-source code that anyone can inspect. You keep full control of your assets, which gets rid of that company-specific risk. But now you're exposed to smart contract risk, where a bug or an exploit in the code itself could lead to a loss.

The safest play is always diversification. Never, ever put all your capital onto a single platform. Spreading your stablecoins across several well-audited and reputable protocols dramatically lowers the damage if any one of them fails.

Why Are Stablecoin Interest Rates So Much Higher Than Banks?

The massive gap between stablecoin yields and what traditional banks offer boils down to two things: insane demand and radical efficiency. The crypto market is absolutely starved for stablecoin liquidity.

Traders and institutions are constantly looking to borrow stablecoins for all sorts of reasons:

Leveraged Trading: To juice up their trading positions.

Arbitrage: To cash in on tiny price differences between exchanges.

Providing Liquidity: To earn fees elsewhere in the sprawling DeFi ecosystem.

This red-hot demand means borrowers are willing to pay a premium for capital, and that premium gets passed directly to you as interest.

Plus, DeFi protocols run on fumes compared to traditional banks. There are no marble lobbies, no massive payrolls, and no creaky, old-school banking systems to pay for. This super-lean operational model means a much bigger slice of the lending profits goes straight back to the depositors. It's that powerful one-two punch of high demand and lean operations that makes it possible to earn interest on stablecoins at rates banks just can't touch.

Ready to stop researching and start earning? Yield Seeker takes the guesswork out of finding the best stablecoin yields. Our AI-driven platform continuously scans the top DeFi protocols on BASE to automatically place your funds in the highest-earning opportunities, all without lockups or hidden fees. Get started in seconds and let our technology do the work for you. Discover effortless crypto income today at https://yieldseeker.xyz.